Personal Income Tax (PIT) finalization is the annual reconciliation foreign employees must complete by March 31 (employer-authorized) or April 30 (self-filed) of the following year—or 45 days before departure (Law 109/2025/QH15, Article 47). Late filing triggers 0.03% daily interest on overdue tax plus administrative penalties. The primary compliance risks: residency determination errors under the 183-day rule, split-year 2026 bracket calculations, and Double Taxation Agreement (DTA) claim denials.

Permanent residence cardholders and individuals with qualifying long-term leases are tax residents regardless of actual presence days. Foreign Legal Representatives face exit suspension risks when company tax debts remain unpaid, and Chief Representatives must finalize PIT on offshore salaries when they meet the 183-day test. Departing expats must finalize 45 days before exit to obtain tax clearance for work permit cancellation.

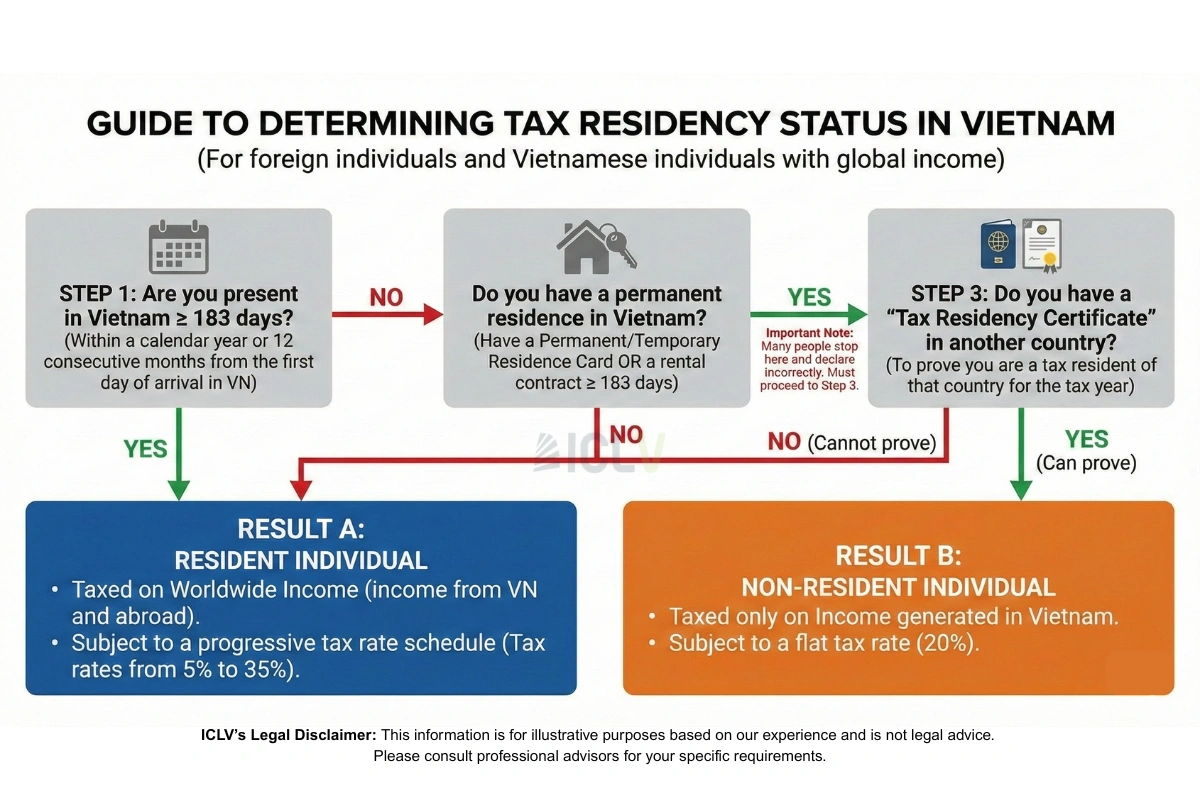

Tax Residency Determination: The 183-Day Rule

Summary of current Vietnamese tax residency rules and PIT framework; does not replace advice from qualified tax advisers or the tax authority.

You become a Vietnam tax resident if you meet ANY of these criteria:

- Physical presence in Vietnam for 183 days or more within a calendar year, OR

- Physical presence for 183 days or more within any consecutive 12-month period starting from your first arrival date, OR

- You register a permanent residence in Vietnam (rare for expats), OR

- You lease a residence in Vietnam with a contract term of 183 days or more—applies even if you don’t occupy the residence continuously

Residents pay progressive rates (5%-35%) on worldwide income after deductions. Non-residents pay a flat 20% on Vietnam-sourced employment income only—no deductions allowed.

The General Department of Taxation counts any part of a 24-hour period as a full presence day—arrival at 11:50 PM counts as Day 1. GDT reviews entry/exit stamps and recalculates presence days including previously excluded business travel (Law 109/2025/QH15, Article 2, guided by Circular 111/2013/TT-BTC Article 1).

Tax year defaults to calendar year, but expats arriving mid-year can elect a 12-month period from arrival by notifying the Tax Authority within 30 days.

| ⚠️ COMPLIANCE ALERT: Expats with Vietnam permanent residence cards are TAX RESIDENTS from day one—progressive brackets apply regardless of actual presence days under Law 109/2025/QH15 |

|---|

Dual-status scenarios occur when an expat transitions from non-resident to resident mid-year. Income before residency is taxed at 20%, post-residency income follows progressive brackets. Retroactive residency determination leads to back-tax assessments plus 0.03% daily interest under Law on Tax Administration 2019.

Tax residency status intersects with employment contract structure and work permit validity—for the full employer compliance framework, see Vietnam employment law and HR compliance for FDI companies.

PIT Finalization Process: Deadlines & 2026 Law Changes

Expats must file Form 02/QTT-TNCN by March 31 of the following year (employer-authorized) or April 30 (self-filed) for calendar-year filers, or within 45 days before departure for mid-year exits. Because these dates overlap heavily with other statutory deadlines, verify your timeline against our annual HR compliance calendar. The 45-day pre-departure deadline is strictly enforced—processing takes 15-20 business days minimum, and tax clearance certificates are required for work permit cancellation (Law 109/2025/QH15, Article 47).

Finalization splits between employer-managed and self-filed. Employer-managed applies when the expat receives income from a single Vietnamese employer who withholds PIT monthly. Self-filing is mandatory for multiple income sources, non-withholding income, or when claiming deductions the employer didn’t process.

Who Must Self-File vs Employer-Managed Finalization

Employer Authorization:

- ONE employer in Vietnam, all income is salary from that employer

- Monthly withholding covered 100% of Vietnam tax liability

- Employer files Form 02/QTT-TNCN by March 31 of the following year

Self-Finalization - Mandatory when:

- Multiple employers in Vietnam

- Income from outside Vietnam (foreign salary, dividends, rental income)

- Non-withholding income (freelance fees, director fees)

- Departing mid-year

- Annual income exceeds VND 100 million with non-employment income

Contract type determines whether employer-managed or self-finalization applies—review Vietnam labor contract types and written contract requirements for PIT withholding implications.

Critical trap: Expats with worldwide income often assume employer withholding equals finalization complete. If you earned salary from your home country employer while working in Vietnam, you MUST self-finalize and declare that foreign income. Employer authorization does not cover it. C-level executives and Legal Representatives face higher scrutiny on worldwide income.

Special Roles Attention Beyond standard employees, Foreign Legal Representatives and Chief Representatives of Representative Offices must strictly adhere to finalization rules. These roles often face higher scrutiny regarding “Global Income” and are subject to immediate exit suspension if personal tax liabilities are outstanding.

| Scenario | Deadline | Authority |

|---|---|---|

| Employer finalizes (authorized) | By March 31 of the following year | Circular 111/2013/TT-BTC (amended), Law 109/2025/QH15 |

| Individual self-finalizes | By April 30 of the following year | Law on Tax Administration 2019 Article 44 |

| Foreigner departing Vietnam | Before exit / within 45 days of contract termination | Circular 111/2013/TT-BTC (amended), Law 109/2025/QH15 |

| First-year resident (arrival mid-year) | By April 30 after first 12-month period ends | Circular 111/2013/TT-BTC (amended), Law 109/2025/QH15 |

2026 Progressive Tax Brackets & Required Documents

The new PIT Law 109/2025/QH15 consolidates seven tax brackets into five tiers—salary/wage provisions apply from the 2026 tax period (January 1, 2026), with the full law effective July 1, 2026. Personal deductions increase from VND 11 million to VND 15.5 million monthly, dependent deductions from VND 4.4 million to VND 6.2 million per qualified dependent, effective January 1, 2026.

The new bracket change directly impacts gross-to-net calculations for every employee—see employer payroll costs and gross-to-net calculation guide for worked examples with 2026 deductions.

Form 02/QTT-TNCN requires:

- Annual PIT withholding statement from employer (Form 11-TNCN)

- Proof of dependent registrations if claiming dependent deductions

- Insurance premium receipts if claiming voluntary insurance deductions

- For DTA claims: Tax residency certificate from home country + DTA notification form filed at assignment start

- For departing expats: Exit flight booking or contract termination letter + work permit documents

Tax clearance certificate (Form 08-MST) is required for work permit cancellation. PIT refunds are processed by the tax authority after review and are typically paid via bank transfer—processing time can vary by locality and case, so taxpayers should allow for administrative review rather than relying on a fixed timeframe.

Employees near minimum wage floors benefit most from the increased personal deductions—see Vietnam’s 2026 minimum wage rates and downstream payroll impact for bracket interaction effects.

Common Expat Scenarios: Practical Application

Scenario 1: Mid-Year Arrival

You arrived July 1, Year 1, worked until December 31 (184 days). You’re a resident for Year 1 (183+ days under Circular 111/2013/TT-BTC Article 1). File by March 31, Year 2. Declare income from July 1-December 31, Year 1. Apply progressive rates and claim family deductions for 6 months present.

Scenario 2: Mid-Year Departure

You terminate May 31, Year 2 after arriving January 1, Year 1. Year 2 presence: 151 days (non-resident unless lease triggers residency). File within 45 days (by July 15, Year 2) under Law 109/2025/QH15, Article 47. If non-resident, pay flat 20%. If resident, apply progressive rates.

Steps: (1) Notify employer immediately, (2) Gather documents (labor contract, termination decision, tax withholding receipts, passport, work permit documents), (3) File Form 02/QTT-TNCN, (4) Obtain tax clearance (Form 08-MST), (5) Employer cancels work permit.

Tax clearance is required before work permit cancellation—confirm the full cancellation sequence in Vietnam work permit requirements and FDI compliance procedures.

Scenario 3: Multiple Employers

You worked for Company A (January-June) and Company B (July-December), both withheld PIT. Self-finalization mandatory under Law on Tax Administration 2019 Article 44. Aggregate income, apply progressive rates to combined taxable income. Documents: tax withholding certificates from both companies, labor contracts, passport.

Special Compliance for Legal Representatives & Chief Representatives

C-level executives, Legal Representatives, and Chief Representatives face higher GDT scrutiny due to complex compensation packages. Key obligations:

Worldwide Income & Split-Salary Arrangements

Tax residents owe PIT on worldwide income regardless of where salary is paid. “Split-salary” arrangements—part paid in Vietnam, part offshore—are monitored closely. The Tax Authority cross-checks work permit validity against declared income: 12 months of Vietnam employment but only 6 months declared triggers audit. Full compensation including bonuses, stock options, and parent company allowances must be declared (Law 109/2025/QH15, Article 2).

Chief Representatives of Representative Offices meeting the 183-day test must declare offshore salary—the belief that RO salaries are tax-exempt is incorrect. Missing filings trigger 20% penalties plus 0.03% daily interest under Law on Tax Administration 2019.

Tax-Exempt Benefits & Exit Suspension

Non-taxable benefits under Circular 111/2013/TT-BTC (paid directly to providers with invoices): school fees (preschool–high school in Vietnam), housing rental (capped at 15% of taxable income), one annual home-leave ticket, and relocation costs. Example: VND 100M gross salary with VND 40M employer-paid rent → only VND 15M taxable (15% cap) → VND 8.75M monthly savings at 35% bracket.

Exit suspension risk: When company tax debts remain overdue, the tax authority may request temporary exit suspension for Legal Representatives under Law on Tax Administration 2019. Before international travel, verify all corporate tax is current—once the exit block triggers, you have no negotiating leverage.

Compliance Risks & Common Failures

Residency misclassification creates the largest exposure—employers incorrectly exclude business travel days or miss permanent residence status. GDT recalculates presence days via immigration stamps, resulting in back-taxes plus 20% penalty plus 0.03% daily interest under Law on Tax Administration 2019.

Late finalization blocks work permit cancellation for departing expats—you can’t leave without tax clearance but can’t obtain clearance without finalizing. Departure without finalization creates employer liability: the employer remains jointly liable for unpaid PIT if the employee is unreachable—withhold final salary until tax clearance is obtained.

For DTA relief, tax authorities require timely notification and supporting documentation under the applicable treaty. Late or incomplete submissions can lead to denial—whether retroactive relief is available depends on the relevant DTA procedures.

Proper termination procedures prevent employer PIT exposure—see employee termination legal grounds and severance calculation. Departing expats must coordinate PIT finalization with social insurance refund timing—see Vietnam social insurance 2026 rates and expat refunds.

PIT finalization is one element of year-end compliance—employers must also reconcile trade union fee obligations on the social insurance salary base and verify PIT treatment of holiday overtime premiums and unused leave payouts before closing annual payroll accounts.

Disclaimer: This guide provides general information on Vietnam PIT finalization procedures current as of March 2026 and does not constitute legal or tax advice. Consult qualified tax advisers for case-specific guidance.

Indochina Link Vietnam provides end-to-end PIT finalization services for FDI companies: residency determination, DTA optimization, eTax registration, and departure compliance.

| Foreigner departing Vietnam | Before exit / within 45 days of contract termination | Circular 111/2013/TT-BTC (amended), Law 109/2025/QH15 | | First-year resident (arrival mid-year) | By April 30 after first 12-month period ends | Circular 111/2013/TT-BTC (amended), Law 109/2025/QH15 |

2026 Progressive Tax Brackets & Required Documents

The new PIT Law 109/2025/QH15 consolidates seven tax brackets into five tiers—salary/wage provisions apply from the 2026 tax period (January 1, 2026), with the full law effective July 1, 2026. Personal deductions increase from VND 11 million to VND 15.5 million monthly, dependent deductions from VND 4.4 million to VND 6.2 million per qualified dependent, effective January 1, 2026.

The new bracket change directly impacts gross-to-net calculations for every employee—see employer payroll costs and gross-to-net calculation guide for worked examples with 2026 deductions.

Form 02/QTT-TNCN requires:

- Annual PIT withholding statement from employer (Form 11-TNCN)

- Proof of dependent registrations if claiming dependent deductions

- Insurance premium receipts if claiming voluntary insurance deductions

- For DTA claims: Tax residency certificate from home country + DTA notification form filed at assignment start

- For departing expats: Exit flight booking or contract termination letter + work permit documents

Tax clearance certificate (Form 08-MST) is required for work permit cancellation. PIT refunds are processed by the tax authority after review and are typically paid via bank transfer—processing time can vary by locality and case, so taxpayers should allow for administrative review rather than relying on a fixed timeframe.

Employees near minimum wage floors benefit most from the increased personal deductions—see Vietnam’s 2026 minimum wage rates and downstream payroll impact for bracket interaction effects.

Common Expat Scenarios: Practical Application

Scenario 1: Mid-Year Arrival

You arrived July 1, Year 1, worked until December 31 (184 days). You’re a resident for Year 1 (183+ days under Circular 111/2013/TT-BTC Article 1). File by March 31, Year 2. Declare income from July 1-December 31, Year 1. Apply progressive rates and claim family deductions for 6 months present.

Scenario 2: Mid-Year Departure

You terminate May 31, Year 2 after arriving January 1, Year 1. Year 2 presence: 151 days (non-resident unless lease triggers residency). File within 45 days (by July 15, Year 2) under Law 109/2025/QH15, Article 47. If non-resident, pay flat 20%. If resident, apply progressive rates.

Steps: (1) Notify employer immediately, (2) Gather documents (labor contract, termination decision, tax withholding receipts, passport, work permit documents), (3) File Form 02/QTT-TNCN, (4) Obtain tax clearance (Form 08-MST), (5) Employer cancels work permit.

Tax clearance is required before work permit cancellation—confirm the full cancellation sequence in Vietnam work permit requirements and FDI compliance procedures.

Scenario 3: Multiple Employers

You worked for Company A (January-June) and Company B (July-December), both withheld PIT. Self-finalization mandatory under Law on Tax Administration 2019 Article 44. Aggregate income, apply progressive rates to combined taxable income. Documents: tax withholding certificates from both companies, labor contracts, passport.

Special Compliance for Legal Representatives & Chief Representatives

C-level executives, Legal Representatives, and Chief Representatives face higher GDT scrutiny due to complex compensation packages. Key obligations:

Worldwide Income & Split-Salary Arrangements

Tax residents owe PIT on worldwide income regardless of where salary is paid. “Split-salary” arrangements—part paid in Vietnam, part offshore—are monitored closely. The Tax Authority cross-checks work permit validity against declared income: 12 months of Vietnam employment but only 6 months declared triggers audit. Full compensation including bonuses, stock options, and parent company allowances must be declared (Law 109/2025/QH15, Article 2).

Chief Representatives of Representative Offices meeting the 183-day test must declare offshore salary—the belief that RO salaries are tax-exempt is incorrect. Missing filings trigger 20% penalties plus 0.03% daily interest under Law on Tax Administration 2019.

Tax-Exempt Benefits & Exit Suspension

Non-taxable benefits under Circular 111/2013/TT-BTC (paid directly to providers with invoices): school fees (preschool–high school in Vietnam), housing rental (capped at 15% of taxable income), one annual home-leave ticket, and relocation costs. Example: VND 100M gross salary with VND 40M employer-paid rent → only VND 15M taxable (15% cap) → VND 8.75M monthly savings at 35% bracket.

Exit suspension risk: When company tax debts remain overdue, the tax authority may request temporary exit suspension for Legal Representatives under Law on Tax Administration 2019. Before international travel, verify all corporate tax is current—once the exit block triggers, you have no negotiating leverage.

Compliance Risks & Common Failures

Residency misclassification creates the largest exposure—employers incorrectly exclude business travel days or miss permanent residence status. GDT recalculates presence days via immigration stamps, resulting in back-taxes plus 20% penalty plus 0.03% daily interest under Law on Tax Administration 2019.

Late finalization blocks work permit cancellation for departing expats—you can’t leave without tax clearance but can’t obtain clearance without finalizing. Departure without finalization creates employer liability: the employer remains jointly liable for unpaid PIT if the employee is unreachable—withhold final salary until tax clearance is obtained.

For DTA relief, tax authorities require timely notification and supporting documentation under the applicable treaty. Late or incomplete submissions can lead to denial—whether retroactive relief is available depends on the relevant DTA procedures.

Proper termination procedures prevent employer PIT exposure—see employee termination legal grounds and severance calculation. Departing expats must coordinate PIT finalization with social insurance refund timing—see Vietnam social insurance 2026 rates and expat refunds.

PIT finalization is one element of year-end compliance—employers must also reconcile trade union fee obligations on the social insurance salary base and verify PIT treatment of holiday overtime premiums and unused leave payouts before closing annual payroll accounts.

Disclaimer: This guide provides general information on Vietnam PIT finalization procedures current as of March 2026 and does not constitute legal or tax advice. Consult qualified tax advisers for case-specific guidance.

Indochina Link Vietnam provides end-to-end PIT finalization services for FDI companies: residency determination, DTA optimization, eTax registration, and departure compliance.