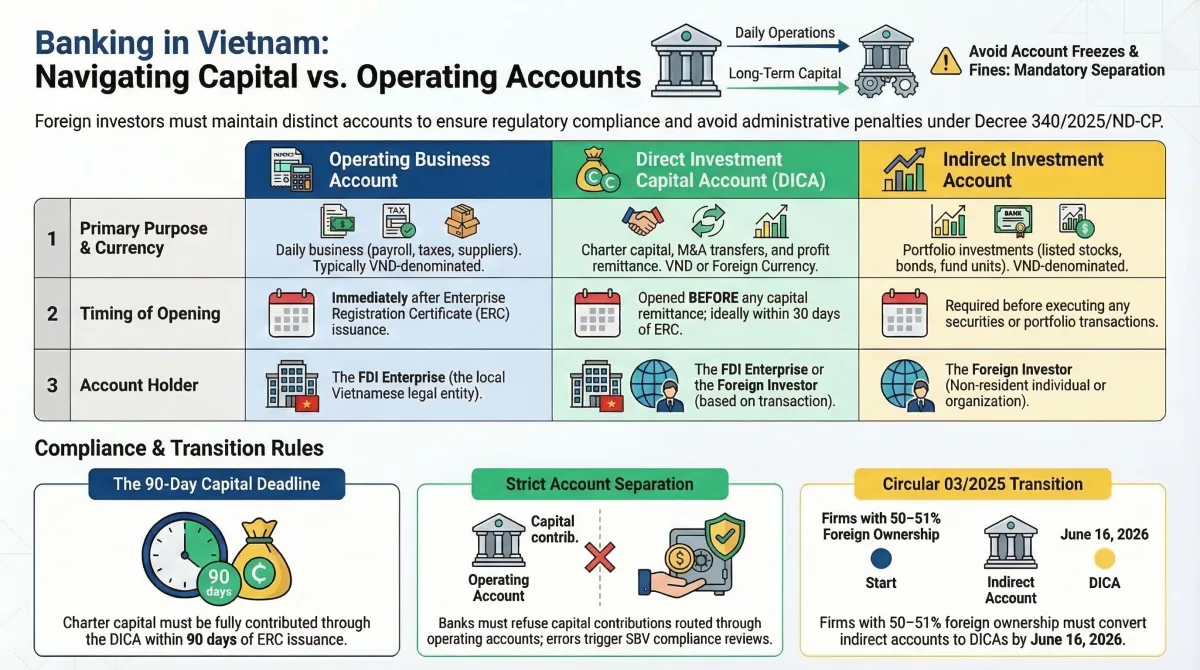

Every foreign-invested enterprise in Vietnam must open bank accounts immediately after receiving the Enterprise Registration Certificate (ERC). Three accounts form the foundation: a Direct Investment Capital Account (DICA) for charter capital under Circular 06/2019/TT-NHNN, a VND payment account for daily operations, and a foreign currency payment account for cross-border transactions.

Get the account structure wrong, and the consequences stack up fast. Capital contributions routed through the wrong account trigger administrative penalties under Decree 340/2025/ND-CP (VND 10–250 million / ~USD 400–10,000). Miss the 90-day contribution deadline because accounts opened late, and the company faces VND 30–50 million fines plus potential ERC revocation.

The following sections cover which accounts FDI companies need, how to open them, and the compliance rules that keep the capital structure clean.

Executive Key Takeaways

- DICA: Mandatory for all FDI capital flows—charter capital, M&A transfers, profit remittances. One DICA per currency at one SBV-licensed bank (Circular 06/2019/TT-NHNN)

- Payment Accounts: VND for daily operations (unlimited accounts, multiple banks). Foreign currency for import/export and overseas payments

- 90-Day Deadline: Capital must flow through DICA within 90 days of ERC issuance (Law on Enterprises 2020). Late contribution triggers charter capital reduction or ERC revocation

- Account Separation: Never mix capital and operating funds. SBV monitors DICAs specifically for investment compliance

1. Bank Accounts Every FDI Company Needs

1.1 Direct Investment Capital Account (DICA)

The DICA is the mandatory capital account—the only legally valid channel for charter capital contributions, capital transfers (M&A), and profit/dividend remittances abroad. Circular 06/2019/TT-NHNN governs this account exclusively for FDI enterprises.

Key constraints most investors don’t expect:

- One DICA per currency denomination at one SBV-licensed bank. Choose VND or a foreign currency—you can’t split across banks

- Only authorized banks may host DICAs. International banks (HSBC, Standard Chartered, Citibank) and major Vietnamese banks (Vietcombank, Techcombank, VPBank) hold SBV licenses. Verify your preferred bank’s authorization before committing

- Switching banks requires closing the existing DICA entirely, then re-opening at the new bank with the full document package. Budget 2–3 weeks for the transition

What flows through the DICA:

| Transaction | Direction |

|---|---|

| Charter capital contribution | Inbound |

| Capital increase | Inbound |

| Foreign loan disbursement (principal + interest) | Both |

| Dividend/profit remittance to foreign parent | Outbound |

| Capital transfer (M&A proceeds) | Both |

What does NOT flow through the DICA: payroll, supplier payments, tax remittances, rent, or any daily operating expense. These belong in the payment accounts.

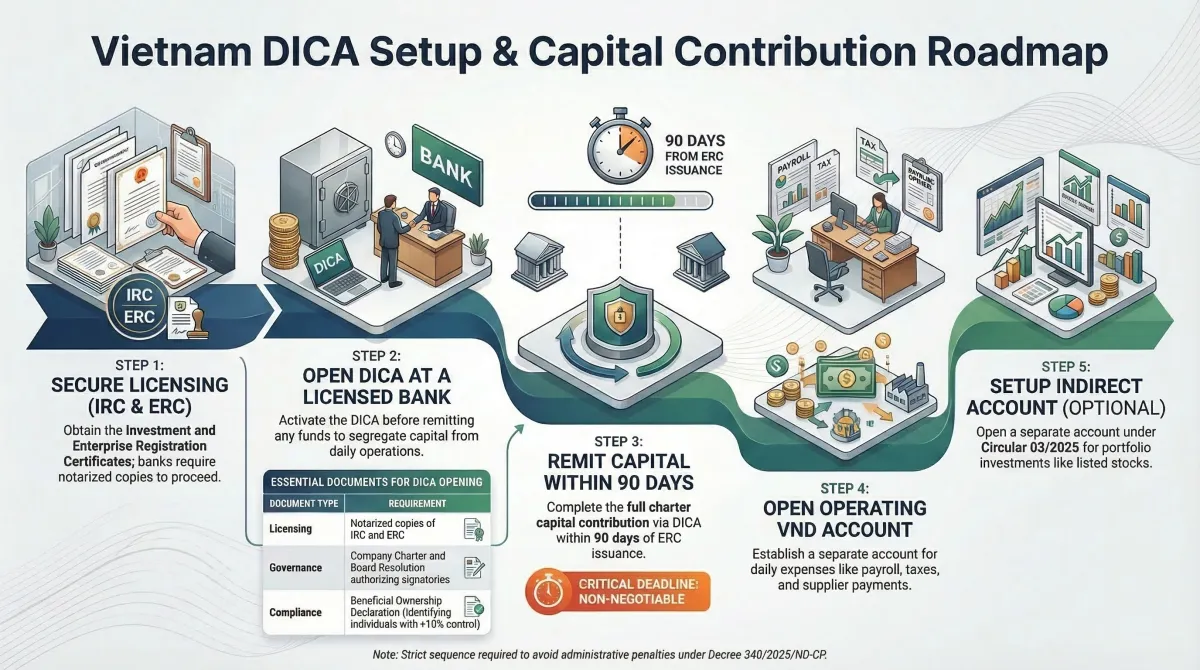

1.2 VND Payment Account (Operating Account)

The VND payment account handles all domestic business transactions. Unlike the DICA, FDI companies can open multiple VND accounts at different banks—no restrictions on quantity or institution.

This account covers:

- Revenue collection from domestic sales

- Payroll and bonus payments

- Supplier and contractor payments

- Tax remittances (VAT, CIT, PIT)

- Rent, utilities, and operating expenses

VND payment accounts earn interest according to the bank’s current rate structure. Most FDI companies open at least two: one primary operating account and one payroll-dedicated account for cleaner audit trails.

1.3 Foreign Currency Payment Account

FDI companies involved in import/export, overseas supplier payments, or cross-border service contracts need a foreign currency payment account. Unlike the DICA (which is a capital account), this is a payment account for trade-related foreign currency flows.

Permitted transactions include:

- Export revenue in foreign currency

- Import payments for goods and services

- Overseas staff allowances and salary payments

- Fee and interest payments to foreign parties

Exchange obligation: Vietnamese law generally requires FDI enterprises to sell foreign currency proceeds through an authorized bank when making domestic payments. FDI enterprises can’t hold unlimited foreign currency for VND-denominated expenses—the bank converts at the prevailing rate.

Foreign currency payment accounts offer both demand deposit (interest calculated daily, credited monthly) and fixed deposit options (interest paid at maturity). If you don’t withdraw at maturity, the bank rolls the deposit into a new term or transfers to a demand account.

1.4 Loan Accounts

If the FDI enterprise borrows foreign-currency loans and the loan currency differs from the DICA’s denomination, a separate loan account must be opened at an authorized bank. Medium and long-term foreign loans require SBV registration before disbursement.

Each bank sets its own requirements depending on the loan type (cash, fixed assets, working capital). This is a specialized account—most standard FDI setups don’t need it until expansion financing.

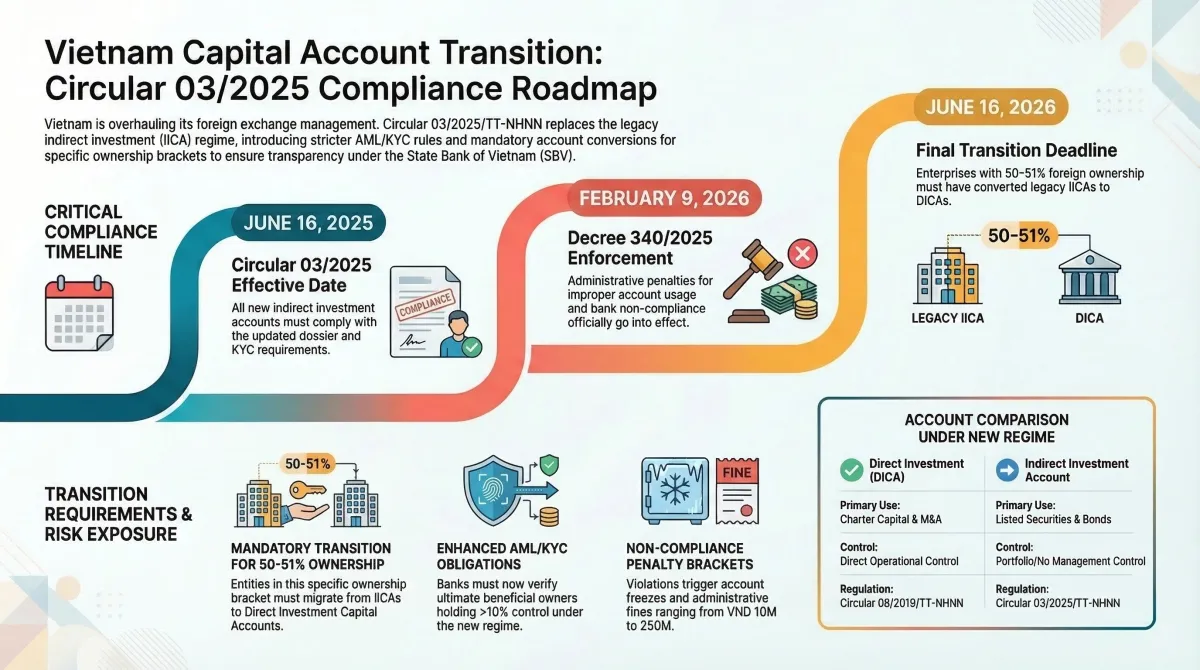

Note: If your FDI company engages in portfolio investment—purchasing listed shares, bonds, or fund units—you need a separate indirect investment account under Circular 03/2025/TT-NHNN (effective June 16, 2025). This is distinct from the DICA and rarely applies to standard FDI operations. See the FAQ section for details.

2. Opening the DICA: Step-by-Step

The sequence matters. Open accounts out of order, and you miss statutory deadlines.

2.1 Document Checklist

Prepare these before visiting the bank:

- IRC and ERC (notarized copies)

- Company charter (notarized)

- Legal representative identification (passport for foreigners, ID card for Vietnamese residents)

- Board resolution authorizing DICA opening and designating authorized signatories

- Beneficial ownership declaration identifying all individuals with >10% ownership or control (per Law on Anti-Money Laundering 2022 and Circular 27/2025/TT-NHNN)

- Proof of registered office address

The #1 cause of delays: incomplete or unclear beneficial ownership information. Banks must verify ultimate beneficial owners—they’ll refuse to open the account if they can’t complete this verification.

2.2 Timeline & Deadlines

| Milestone | Deadline | Why It Matters |

|---|---|---|

| Open DICA | Within 30 days of ERC | Buffer time for processing delays |

| Complete capital contribution | Within 90 days of ERC | Statutory deadline (Law on Enterprises 2020, Articles 47/75/113) |

| Obtain bank confirmation | Within 5 days of contribution | Required for audit and Department of Finance (formerly DPI) reporting |

| Submit to Department of Finance (formerly DPI) | Within 10 days of confirmation | Decree 01/2021/ND-CP, Article 44 |

| ⚠️ COMPLIANCE ALERT: The 90-day deadline is calculated from ERC issuance, NOT from IRC issuance. Many investors confuse these dates. |

Banks in HCMC typically process DICA applications within 5–10 business days if all documents are complete. Hanoi banks run similar timelines. Factor in an extra 3–5 days for KYC verification if your ownership structure involves multiple layers or offshore holding companies.

2.3 Choosing a Bank

The bank choice is more constrained than most investors expect. Only SBV-licensed banks can host DICAs, and once opened, switching means closing and re-opening with full documentation.

Practical selection criteria:

- International banks (HSBC, Standard Chartered, Citibank): Better for companies with parent-company banking relationships, multi-currency needs, and large cross-border transfers. Higher account minimums, more rigorous KYC

- Major Vietnamese banks (Vietcombank, Techcombank, VPBank, MB Bank): Faster local processing, lower fees, better integration with Vietnamese tax and customs systems. Preferred for companies with primarily domestic operations

- Industrial zone banks: Some IZ management boards have preferred banking partners with streamlined DICA processes for zone tenants

The LLC governance structure—specifically whether the company is a single-member or multi-member LLC—affects the board resolution and authorized signatory requirements for the DICA application.

Ask the bank specifically: (1) Are you licensed to open DICAs? (2) What is the DICA processing timeline? (3) What are the capital contribution wire transfer requirements? Get exact wiring syntax instructions before the first transfer.

3. Account Separation & Compliance

3.1 The Golden Rule: Never Mix Capital and Operating Funds

SBV monitors DICAs specifically for investment capital compliance. Capital contributions routed through operating accounts—intentionally or accidentally—create immediate regulatory exposure.

| Transaction Type | Correct Account | Legal Basis |

|---|---|---|

| Charter capital contribution | DICA | Circular 06/2019/TT-NHNN |

| Capital transfer (M&A) | DICA | Circular 06/2019/TT-NHNN |

| Dividend/profit remittance abroad | DICA | Circular 06/2019/TT-NHNN |

| Payroll, suppliers, taxes | VND Payment Account | Bank internal regulations |

| Import/export payments | FC Payment Account | Circular 06/2019/TT-NHNN |

Banks are required to refuse capital contributions routed through operating accounts. If such transactions are processed, both the enterprise and the bank face administrative sanctions.

3.2 Penalties for Getting It Wrong

Administrative penalties under Decree 340/2025/ND-CP (effective February 9, 2026) range from VND 10–250 million (~USD 400–10,000) for improper account usage, AML/KYC non-compliance, and banks failing to maintain proper account regulations.

Red flags that trigger SBV reviews:

- Capital amount doesn’t match IRC-declared charter capital

- Capital routed through multiple accounts before reaching DICA

- Dividend remittances without audited distributable profits

- Frequent account closures and re-openings

The wiring syntax trap: When transferring capital from abroad, the remittance message must state exactly: “Charter capital contribution by [Member Name] to [Company Name, Tax Code].” If the wire says “Loan,” “Project Fund,” or just “Transfer,” the bank can’t legally record it as equity—forcing a refund, re-send, and double forex conversion losses.

3.3 Compliance Priorities

- Open DICA within 30 days of ERC issuance for buffer time

- Maintain strict account separation—never route capital through operating accounts

- Complete AML/KYC thoroughly, including beneficial ownership declarations

- Keep a compliance file linking all account documents (IRC, ERC, resolutions, remittance receipts)

- Coordinate profit remittances with your tax advisor—banks require tax clearance certificates before processing outbound transfers

- Structure DICA signatory authority carefully when using appointed resident representatives—the representative’s signing power over capital accounts creates real financial exposure

4. Next Steps

Proper account structuring is the foundation of FDI compliance. The framework is straightforward: DICA for capital flows, payment accounts for daily business, separate foreign currency accounts for cross-border trades. Mixing account types creates regulatory exposure that cascades across SBV, tax authorities, and auditors.

- Complete the IRC/ERC registration process before approaching your bank—no bank opens a DICA without these certificates

- For the complete Vietnam market entry roadmap, including entity selection, tax registration, and profit repatriation, see our pillar guide

- If your entity type involves multiple foreign investors, each investor’s contribution flows through the same DICA but requires separate remittance documentation

- Coordinate corporate e-ID registration alongside banking setup—both require legal representative presence

Indochina Link Vietnam assists with compliant banking setup, DICA registration, and ongoing regulatory monitoring. Our FDI reporting service covers DICA management alongside statutory accounting obligations. Contact us to ensure your capital account structure meets current SBV requirements.

Important: This information reflects regulations current as of March 2026. Vietnamese banking and foreign exchange regulations change frequently. For specific situations, consult qualified legal and tax professionals licensed in Vietnam.