Vietnam offers five market entry structures for foreign investors: FDI companies (LLC or JSC), representative offices, branches of foreign traders, and employer-of-record (EOR) arrangements—each governed by Law on Investment 2025 (No. 143/2025/QH15, effective March 1, 2026) and Law on Enterprise 2020 (as amended by Laws 29/2025 and 76/2025, effective July 1, 2025).

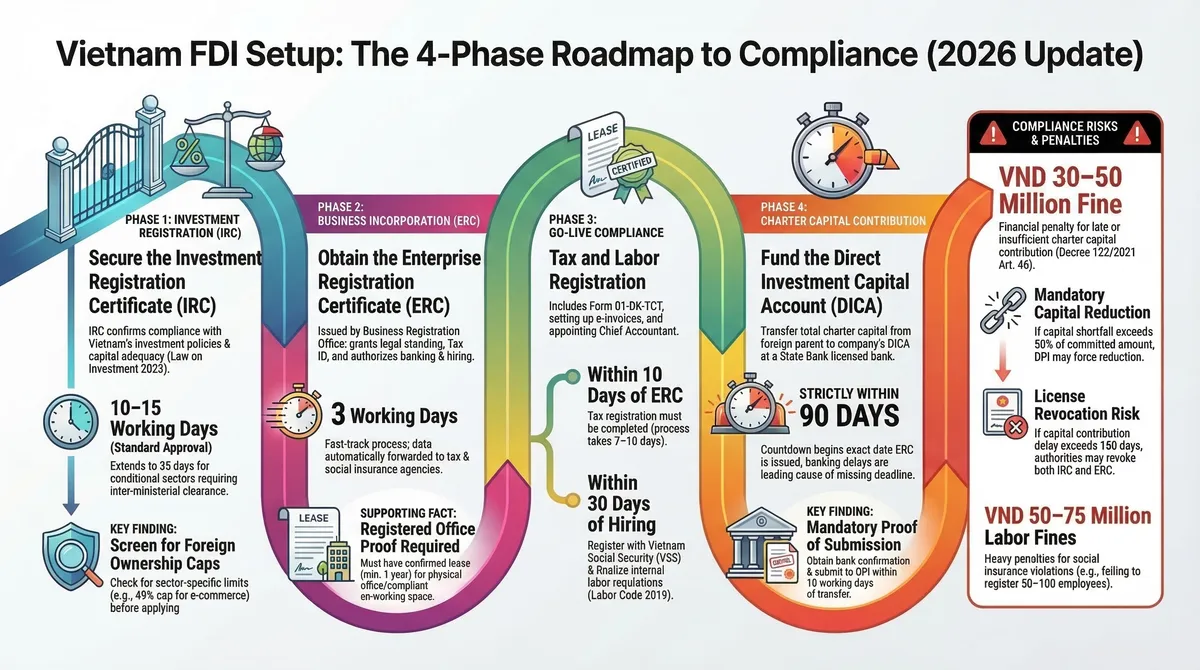

Vietnam attracted USD 38.23 billion in FDI in 2024, ranking third in ASEAN after Singapore and Indonesia. But getting in is the easy part. The standard licensing timeline—IRC (10–15 working days, 35 for conditional sectors) → ERC (3 working days) → tax/labor registration (7–10 days) → charter capital contribution (90-day deadline)—runs 4–6 weeks. Staying compliant after incorporation is where most foreign investors stumble.

Three compliance risks derail more FDI projects than any others: late charter capital contribution (VND 30–50 million / ~USD 1,200–2,000 fines + potential IRC/ERC revocation), social insurance violations (VND 50–75 million / ~USD 2,000–3,000 penalties for 50–100 unregistered employees), and blocked profit remittance from incomplete tax clearance. Register your 3–5 year business activities from day one—narrow scope requires costly amendments (6–8 weeks + VND 5–10 million / ~USD 200–400) and re-approval in conditional sectors.

This guide maps the complete operational lifecycle from entity selection through profit repatriation, with statutory deadlines, penalty exposures, and practical execution requirements.

1. Understanding Your Market Entry Options

Vietnam offers multiple legal structures for foreign investors. The structure choice affects governance, liability, operational scope, and exit flexibility. The two dominant FDI structures are limited liability companies (LLC) and Joint Stock Companies (JSC). Alternative entry modes—representative offices, branches, and EOR arrangements—serve specific, limited purposes.

1.1 Foreign Direct Investment Structures

Limited Liability Company (LLC)

LLCs with foreign ownership in Vietnam are the most popular structure for foreign investors—offering operational flexibility, limited liability protection, and straightforward governance.

- Single-Member LLC: One owner (entity or individual). The owner appoints a Director to manage daily operations.

- Multi-Member LLC: 2–50 members. Governed by a Board of Members, which appoints a Director. Capital changes, charter amendments, and dissolution require member approval per charter-specified voting thresholds.

Capital contribution requirements vary by sector—most have no minimum, while specialized sectors (securities, banking) require VND 42 billion / ~USD 1.7 million or higher. Members’ liability is limited to contributed capital (Law on Enterprise 2020, Article 50).

Joint Stock Company (JSC)

JSCs suit investors planning future capital raises, IPOs, or broad shareholder bases. They require at least 3 founding shareholders and operate under a formal governance structure: General Meeting of Shareholders → Board of Directors → General Director (Law on Enterprise 2020, Articles 111–157). Shares are freely transferable unless restricted by charter provisions.

For most first-time FDI investors, the single-member LLC provides the fastest path to operations. JSCs make sense when you’re planning Series A fundraising or eventual listing on HOSE or HNX.

1.2 Alternative Entry Modes

Representative Office

A representative office—or EOR arrangement for hiring without incorporation—lets foreign companies test the Vietnam market without full entity setup. Representative offices can’t generate revenue, sign commercial contracts, or issue invoices (Decree 07/2016/ND-CP, Article 3). Permitted activities: market research, liaison, and promotion only.

Representative offices operate under 3-year renewable licenses. All expenses must be funded by the foreign parent. Local hiring is restricted to 5 Vietnamese staff without MOLISA approval. For companies that need to hire quickly without entity setup, EOR arrangements offer a faster alternative—typically operational within 1–2 weeks versus 3–4 weeks for a representative office.

Branch of Foreign Trader

A branch can earn revenue from specific activities but requires a sub-license from the relevant ministry—MOIT for trading branches (Decree 09/2018/ND-CP, Article 12). Branches are restricted to import-export, logistics, and support services. The foreign parent bears full liability.

1.3 Structure Comparison and Decision Framework

| Structure | Setup Time | Liability | Operational Scope | Exit Flexibility |

|---|---|---|---|---|

| Single-Member LLC | 4–6 weeks | Limited to contributed capital | Full commercial activities | Moderate (capital transfer requires IRC/ERC amendment) |

| Multi-Member LLC | 4–6 weeks | Limited to contributed capital | Full commercial activities | Moderate (member approval required unless waived) |

| JSC | 6–8 weeks | Limited to share value | Full commercial activities | High (shares freely transferable unless restricted) |

| Representative Office | 3–4 weeks | Foreign parent liable | Non-commercial (liaison, research) | N/A (license expires after 3 years) |

| Branch | 6–10 weeks | Foreign parent liable | Limited (import-export, logistics) | Low (requires sub-license termination) |

| EOR Arrangement | 1–2 weeks | EOR provider liable | Hiring only (no entity) | High (contract termination) |

For detailed governance, capital requirements, and decision criteria, see our LLC vs JSC vs representative office vs branch comparison for foreign investors.

2. The Complete Setup Roadmap: From Market Entry to Operational Compliance

2.1 Phase 1: Pre-Investment & Market Access Check

Screening Business Lines and Foreign Ownership Caps

Vietnam’s conditional business lines and market access requirements determine which sectors foreign investors can enter—and at what ownership level. Foreign ownership caps restrict participation to 49–100% depending on sector (Decree 31/2021/ND-CP, Appendix II).

The Ministry of Planning and Investment (MPI) and MOIT maintain sector-specific guidance, but the rules interact in complex ways—e-commerce platforms remain capped at 49% foreign ownership under Decree 52/2013/ND-CP (not among the 38 conditional business lines abolished by the Law on Investment 2025). Telecommunications services require separate sub-licenses from the Ministry of Information and Communications (Law on Telecommunications 2023, No. 24/2023/QH15).

| Sector | Foreign Ownership Cap | Key Condition |

|---|---|---|

| E-commerce platforms | 49% (may increase with tech transfer) | Sub-license from MOIT |

| Legal services | 51% (joint venture only) | Partnership with Vietnamese law firm |

| Retail distribution (>1 outlet) | 100% (with conditions) | Economic Needs Test (ENT) or sub-license |

| Private education (K-12) | 50% (higher education: 100%) | License from Ministry of Education |

If your target sector has a 49% cap, informal ownership arrangements cannot circumvent it. Vietnamese authorities cross-check ultimate beneficial ownership during IRC review, and from July 2025, UBO disclosure under Decree 168/2025/ND-CP makes informal structures unsustainable.

Retail distribution and FDI trading license requirements deserve special attention—Economic Needs Test approval adds 4–8 weeks to the registration timeline for each retail establishment beyond the first.

⚠️ IMPORTANT: Registering insufficient or overly narrow business lines at incorporation requires later IRC/ERC amendments. This costs 6–8 weeks + VND 5–10 million (~USD 200–400) and re-approval in conditional sectors. Map medium-term activities and register appropriate business lines from day one. Department of Finance (formerly DPI) won’t approve vague descriptions like “consulting services”—you must specify sub-categories (management consulting, IT consulting, tax consulting).

Location and Investment Form Decisions

As of October 1, 2025, location-based CIT incentives for industrial parks have been removed under the amended CIT Law (Law 67/2025/QH15). Current incentives prioritize high-tech sectors (semiconductors, renewable energy, supporting industries) with 10% CIT for 15 years. SMEs receive revenue-based rates: 15% for revenue ≤VND 3 billion (~USD 120,000), 17% for revenue VND 3–50 billion (~USD 120,000–2 million).

Industrial zones offer faster customs clearance and pre-built infrastructure, but location and tax incentive eligibility are now evaluated independently. For projects inside an industrial zone, the Management Board processes the IRC application. Outside industrial zones, the provincial Department of Finance (formerly DPI) serves as the licensing authority.

2.2 Phase 2: Licensing—IRC and ERC

Investment Registration Certificate (IRC)

The IRC confirms the investor’s project complies with Vietnam’s investment policy, sectoral restrictions, and capital adequacy requirements (Law on Investment 2025). Department of Finance (formerly DPI) issues it—or the Management Board for industrial zone projects.

Document Checklist:

- Investment proposal (project description, capital structure, implementation timeline)

- Legal documents of the foreign investor (certificate of incorporation, good standing, audited financials for 2 years)

- Project feasibility study (required if capital exceeds VND 15 billion / ~USD 600,000 or conditional sector)

- Financial capacity proof (bank reference letter, shareholder resolution committing capital)

- Lease agreement or land use rights certificate

- Environmental impact assessment or environmental protection commitment (per Decree 08/2022/ND-CP)

Timeline: Up to 15 working days from complete dossier acceptance; in practice 10 working days under Decree 239/2025/ND-CP (effective September 3, 2025) amending Decree 31/2021/ND-CP. Conditional projects requiring inter-ministerial clearance: 35 working days. In practice, Department of Finance (formerly DPI) often requests clarification within the first week—budget an additional 5–7 days for resubmission.

Enterprise Registration Certificate (ERC)

Once you hold the IRC, apply for the ERC with the Business Registration Office under Department of Finance (formerly DPI) (Law on Enterprise 2020, Articles 26–31). The ERC gives your company legal standing—it assigns your Tax Identification Number (TIN) and authorizes bank accounts, hiring, and contracts.

Timeline: 3 working days from complete dossier (Decree 01/2021/ND-CP, Article 27). The Business Registration Office automatically forwards your information to the tax office, social insurance agency, and statistical office.

Your legal representative carries personal liability beyond their employment scope—understand these risks before making the appointment decision.

For step-by-step IRC and ERC document templates and submission procedures, see our foreign company registration process guide.

| Phase | Authority | Key Document | Statutory Timeline |

|---|---|---|---|

| IRC Application | Department of Finance (formerly DPI) or IZ Management Board | Investment Registration Certificate | 10–15 working days (35 for conditional) |

| ERC Application | Business Registration Office | Enterprise Registration Certificate | 3 working days |

| Tax Registration | GDT / Local Tax Office | Tax Identification Number (TIN) | 10 working days (auto-assigned with ERC) |

| Capital Contribution | SBV-licensed bank | Capital contribution confirmation | 90 days from ERC issuance |

2.3 Phase 3: Go-Live Compliance

Tax Registration and E-Invoice Setup

Tax registration for FDI companies begins automatically—the Business Registration Office forwards ERC data to the General Department of Taxation (GDT). FDI companies must complete tax registration formalities within 10 working days of ERC issuance (Law on Tax Administration 2019, Article 33). This means submitting Form 01-DK-TCT, registering for e-invoice issuance, appointing a chief accountant, and declaring the company’s accounting method.

Don’t wait. The tax office schedules an initial site visit within 5 working days to verify your registered address and accounting readiness. If the company lacks a chief accountant or accounting software, the tax office will issue a compliance notice—delaying the first VAT refund or CIT finalization.

From 2025, enterprises must also complete corporate e-ID registration for digital tax filing and banking transactions.

⚠️ RISK ALERT: As of January 16, 2026, Decree 310/2025/ND-CP significantly revises penalty structures for tax and invoice violations. Delayed VAT or CIT filing can block VAT refunds and profit remittance downstream. Engage your accounting provider before ERC issuance—not after.

Charter Capital Contribution

The deadline is firm: 90 days from ERC issuance (Law on Enterprise 2020, Article 47, Clause 1). Transfer the full charter capital into your company’s Direct Investment Capital Account (DICA) at an SBV-licensed bank. Unlike Singapore—where paid-up capital of SGD 1 is legally sufficient—Vietnam enforces actual capital contribution with real consequences for shortfalls.

Practical execution steps:

- Open the DICA before ERC issuance (requires IRC, draft charter, legal representative appointment)

- Complete KYC process (source of funds declaration, ultimate beneficial ownership disclosure per Circular 06/2019/TT-NHNN)

- Arrange inbound transfers via telegraphic transfer (TT) or contribution in kind (requires independent valuation)

- Obtain the bank’s capital contribution confirmation within 5 working days of funds receipt

- Submit confirmation to Department of Finance (formerly DPI) within 10 working days (Decree 01/2021/ND-CP, Article 44)

Miss this deadline, and you face VND 30–50 million (~USD 1,200–2,000) fines (Decree 122/2021/ND-CP, Article 46). Beyond monetary penalties: Department of Finance (formerly DPI) may require mandatory charter capital reduction if the shortfall exceeds 50%. If the delay exceeds 180 days, Department of Finance (formerly DPI) may revoke your IRC/ERC entirely.

Banks process large inbound transfers slowly—especially through multiple intermediary banks. Pre-fund your capital account before ERC issuance.

Labor and Social Insurance Registration

Within 30 days of hiring your first employee, register with DOLISA and the Vietnam Social Security (VSS) agency (Law on Social Insurance 2024, No. 41/2024/QH15, effective July 1, 2025). You’ll need labor registration forms, internal labor regulations compliant with Labor Code 2019 (Articles 109–126), employee labor contracts, and social insurance registration forms (Form TK1-TS, Form D02-TS).

Written labor contracts are mandatory for all employees (Labor Code 2019, Article 13). No exceptions. The contribution rate: 21.5% (employer) + 10.5% (employee) of gross salary, applying to Vietnamese employees and foreign employees with work permits and contracts exceeding 3 months.

For detailed Vietnam employment law and HR compliance for FDI employers, including work permits, internal labor regulations, and social insurance procedures, see our dedicated guide.

Penalty Warning: Failing to register 50–100 employees for social insurance incurs VND 50–75 million (~USD 2,000–3,000) fines (Decree 168/2025/ND-CP). MOLISA targets this aggressively in manufacturing and logistics sectors.

2.4 Phase 4: Ongoing Operational Compliance

Periodic Tax Filing Obligations

FDI companies enter a continuous compliance cycle once operational. Vietnam’s tax system requires monthly or quarterly filings for VAT, CIT, and PIT, plus annual finalization returns.

Key deadlines:

- VAT: Monthly by the 20th (revenue >VND 50 billion / ~USD 2 million) or quarterly by the 30th of the first month of the following quarter

- CIT: Quarterly provisional payments by the 30th of the first month of the following quarter. Annual finalization by March 31 (Decree 126/2020/ND-CP, Article 44)

- PIT: Monthly withholding by the 20th. Annual finalization by March 31

- FCT: Withholding on payments to foreign contractors: 2–10% VAT + 5–10% CIT depending on service type (Circular 103/2014/TT-BTC)

Transfer pricing documentation is mandatory for related-party transactions exceeding VND 50 billion (~USD 2 million) annually or if reporting consecutive losses (Decree 132/2020/ND-CP, Article 15).

Investment Reporting to Authorities

Foreign-invested enterprises must submit quarterly and annual investment reports to Department of Finance (formerly DPI) and MPI covering capital disbursement, business line implementation, employment compliance, environmental measures, and financials (Law on Investment 2025).

Quarterly reports: due by the 10th of the first month of the following quarter. Annual reports: due by January 31 (Decree 31/2021/ND-CP, Article 58). Late or missing reports cost VND 5–10 million (~USD 200–400) per incident (Decree 122/2021/ND-CP, Article 15). If the project stays inactive for 12 months, Department of Finance (formerly DPI) may suspend or revoke the IRC.

Department of Finance (formerly DPI) cross-checks investment reports against tax filings and social insurance records. Discrepancies trigger compliance reviews.

Mandatory Statutory Audit

All foreign-invested enterprises must have annual financial statements audited by a Vietnam-licensed independent auditing firm, regardless of company size (Law on Independent Audit 2011). The audited report must be submitted with the company’s CIT finalization by March 31. VAS differs significantly from IFRS—parent company IFRS reports are not accepted.

No audit means no profit remittance. Plan for audit engagement by December—auditing firms in Vietnam get fully booked in January–February.

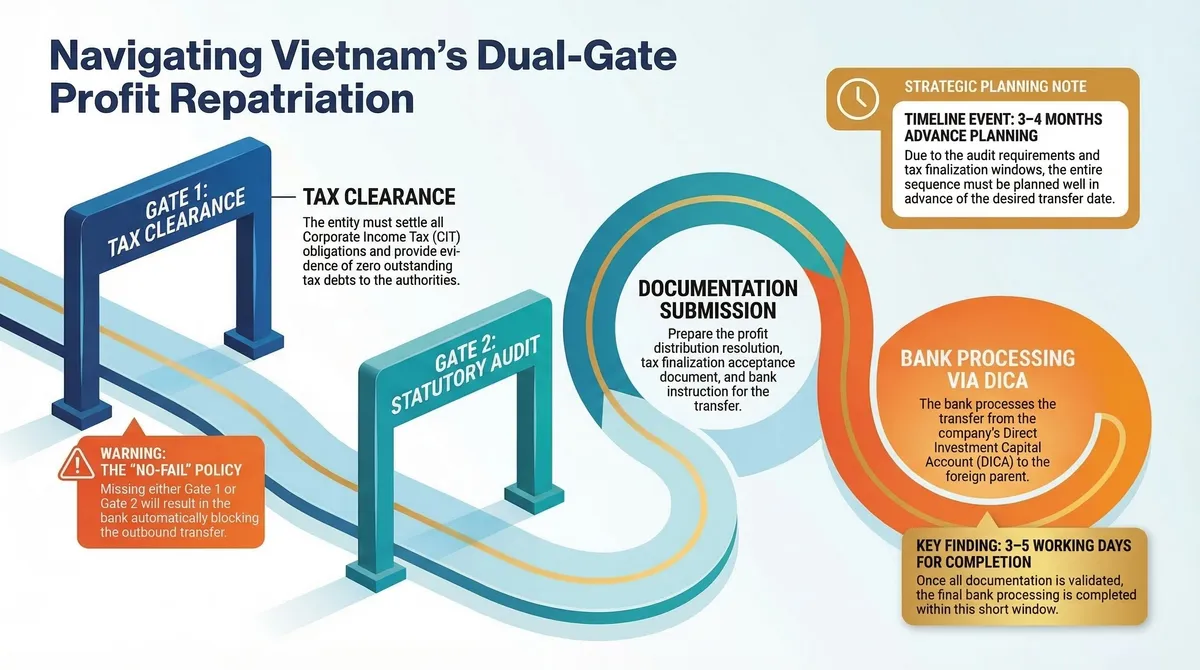

Profit Repatriation and Foreign Exchange

FDI companies can remit profits abroad after satisfying two conditions: all tax obligations settled (CIT finalized, zero outstanding debts) and audited financials confirm distributable profits (Law on Investment 2025). The process requires a profit distribution resolution, tax finalization acceptance document, and bank instruction to transfer from your DICA to the foreign parent.

Banks reject remittance if tax clearance is incomplete or the amount exceeds audited distributable profits. Processing: 3–5 working days once documentation is complete (Circular 06/2019/TT-NHNN). Vietnam’s dual-gate system (tax clearance + audit) means planning your repatriation timeline at least 3–4 months in advance.

| Compliance Milestone | Frequency | Deadline | Penalty for Non-Compliance |

|---|---|---|---|

| VAT Filing | Monthly or Quarterly | 20th of following month / 30th of first month of following quarter | Per Decree 310/2025/ND-CP |

| CIT Provisional Filing | Quarterly | 30th of first month of following quarter | Per Decree 310/2025/ND-CP |

| CIT Annual Finalization | Annual | March 31 (calendar-year companies) | Per Decree 310/2025/ND-CP |

| Investment Reports | Quarterly / Annual | 10th of first month of following quarter / January 31 | VND 5–10 million (~USD 200–400) |

| Audited Financial Statements | Annual | March 31 | VND 10–20 million (~USD 400–800) |

3. Compliance Risks and Enforcement Landscape

Vietnam’s enforcement regime combines statutory penalties with discretionary administrative measures. Understanding the penalty structure—and the inspection practices behind it—helps you prioritize compliance investments.

3.1 Common Compliance Failures

| Violation Type | Penalty Amount | Related Decree |

|---|---|---|

| Late enterprise registration | VND 10–20 million (~USD 400–800) | Decree 122/2021/ND-CP, Article 8 |

| Insufficient charter capital contribution | VND 30–50 million (~USD 1,200–2,000) | Decree 122/2021/ND-CP, Article 46 |

| Late tax registration / filing | Per Decree 310/2025/ND-CP | Consult current schedule |

| Failure to register 50–100 employees for SI | VND 50–75 million (~USD 2,000–3,000) | Decree 12/2022/ND-CP, Article 17 |

Charter capital contribution failure carries the heaviest operational risk beyond the fine itself. Department of Finance (formerly DPI) may require mandatory capital reduction if the shortfall exceeds 50% of committed capital. Delays beyond 180 days risk IRC/ERC revocation. Pre-fund your capital account and complete banking documentation before ERC issuance.

3.2 Inspection Practices

Vietnamese authorities conduct scheduled, ad-hoc, and complaint-triggered inspections.

Tax Audits: GDT targets companies with large VAT refund claims, transfer pricing arrangements, or consecutive losses. Audit cycles run 3–5 years for standard taxpayers, 2–3 years for high-risk sectors (real estate, construction). Focus areas: invoice validity, related-party pricing, management fee deductibility.

Labor Inspections: MOLISA checks labor contracts, social insurance registration, and occupational safety. Inspections spike in Q4 before Tet. The most common violation: unregistered employees or verbal employment agreements.

Investment Compliance Reviews: Department of Finance (formerly DPI) reviews project implementation annually or upon complaints. Red flags: zero revenue for 12+ months, capital disbursement below 50%, unregistered business line activities. Department of Finance (formerly DPI) cross-checks reports against tax filings and social insurance records—discrepancies trigger compliance reviews.

3.3 Risk Scenarios

Case 1: Project Suspension — A Singapore logistics company skipped quarterly reports for three quarters. Department of Finance (formerly DPI)‘s compliance inspection revealed unregistered warehousing activities. Result: IRC suspension for 6 months, VND 45 million in penalties.

Case 2: Blocked Profit Remittance — A Korean manufacturer’s USD 2 million remittance request was rejected because CIT finalization was still under tax audit. Resolution took 3 months, disrupting the parent’s cash flow planning.

Case 3: IRC Revocation — A Hong Kong investor contributed only USD 2 million of USD 10 million committed charter capital within 90 days. Department of Finance (formerly DPI) required capital reduction; non-compliance within 60 days led to IRC/ERC revocation. Sunk costs exceeded USD 500,000.

4. Your Next Steps

Success in Vietnam depends on execution discipline: understanding statutory deadlines, pre-positioning capital, and maintaining continuous compliance across tax, labor, and investment reporting.

- Register broad business lines from day one—amendments cost 6–8 weeks

- Pre-fund your capital account before ERC issuance—banking delays are the #1 cause of missed 90-day deadlines

- Engage your accounting provider before tax registration deadlines

- Submit investment reports on time, every quarter—Department of Finance (formerly DPI) cross-checks everything

- Protect your brand early with trademark registration in Vietnam

- Plan your long-term exit strategy by understanding the complex process of dissolving an FDI company

Indochina Link Vietnam provides Vietnam corporate services from feasibility assessment through post-licensing compliance management. Questions about your specific structure? Contact us for a consultation.

Important: This information reflects regulations current as of March 2026. Vietnamese tax and investment laws change frequently. For specific situations, consult qualified legal and tax professionals licensed in Vietnam.