Foreign legal representatives in Vietnam face administrative penalties reaching VND 150 million (~USD 6,000) for work permit violations (Decree 12/2022/ND-CP, Article 32.4). Tax authorities can also impose exit bans—preventing the legal representative from leaving the country—when the company has unfulfilled tax obligations (Law on Tax Administration 2019, Article 66). The 2025 amendments to the Enterprise Law (Law No. 76/2025/QH15, effective July 1, 2025) expanded personal accountability under Article 13.1, making the legal representative personally liable for damages caused by company violations.

The risks aren’t theoretical. They’re the reason most experienced foreign investors now use a dual legal representative structure to separate daily compliance exposure from strategic control.

What Is a Legal Representative in Vietnam?

A legal representative is an individual officially appointed and registered to act as the legal agent and authorized signatory of a company (Enterprise Law 2020, amended 2025, Article 12). This person has the power to bind the company in legal, financial, and administrative matters—every contract they sign, every tax filing they approve, carries the company’s full legal weight.

Here’s what catches most foreign investors off guard: your internal job title doesn’t matter. CEO, Managing Director, Country Manager—none of these automatically grant legal representative authority. Only registration on the Enterprise Registration Certificate creates this status. Without that registration, you can’t sign tax returns, open bank accounts, or execute contracts on behalf of the company.

Companies can appoint more than one legal representative (Enterprise Law 2020, Article 12.1). This flexibility is what makes the dual representative strategy possible—and it’s the foundation for managing your personal liability exposure. The legal representative role is central to every foreign-invested entity—for the full market entry roadmap, see our complete guide to doing business and company setup in Vietnam.

Who Qualifies as Legal Representative?

Both Vietnamese and foreign nationals qualify as legal representatives if they meet the eligibility requirements under the Enterprise Law 2020, Article 13: at least 18 years old with full legal capacity, resident in Vietnam, holding a managerial position or higher, with no active bankruptcy declarations or business management bans. Civil servants in government agencies cannot serve.

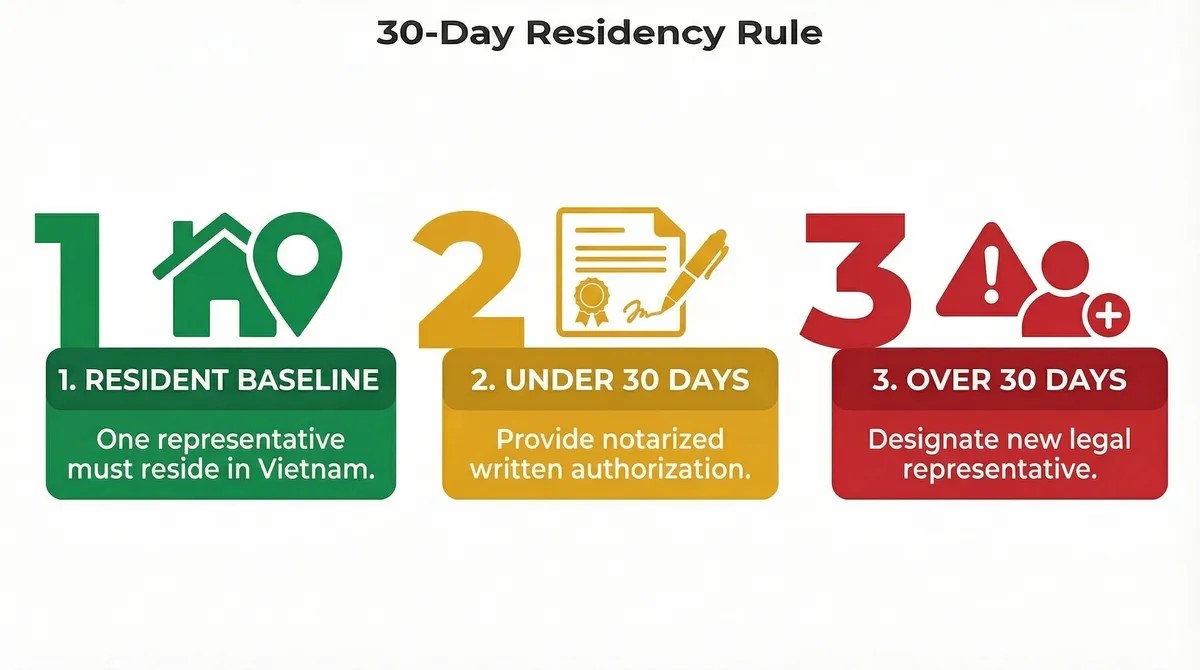

The residency requirement is where things get complicated for foreign investors. Article 12.3 mandates that at least one legal representative must reside in Vietnam continuously. Leave the country for under 30 days? You need a written authorization appointing another Vietnam-based person to act in your place. Exceed 30 days without that authorization? The enterprise must designate a new legal representative entirely.

That 30-day rule creates a real operational burden for foreign investors who travel frequently between Vietnam and their home country or regional offices. Legal representative requirements apply across all entity types, though scope and liability differ—see our comparison of LLC vs JSC vs representative office vs branch structures in Vietnam.

Legal Representative Duties—and Where Liability Starts

Legal representatives must ensure company compliance, represent the enterprise before authorities, and maintain signature authority for all critical filings (Enterprise Law 2020, Article 13). Fail in any of these areas, and personal liability follows.

Compliance responsibility

You’re accountable for the company’s compliance across labor law, tax obligations, social insurance, and work permit requirements. When the company violates regulations, Article 13.1 (as amended in 2025) allows affected parties to hold you personally liable for damages. This isn’t limited to decisions you actively made—it extends to violations that occurred under your watch.

Representation and fiduciary duties

You serve as the company’s official point of contact with government authorities, clients, and partners. This role demands transparent disclosure of personal business interests and stakeholder relationships. Conflicts of interest don’t just create legal risk—they undermine the trust that Vietnamese authorities and banks place in your company’s governance.

Signature authority

Your signature carries legal weight across company establishment, IRC/ERC registration, trading and retail license applications, tax filings (CIT, VAT, social insurance), bank account openings, offshore loan registration, and corporate e-ID authentication. Every signature creates a paper trail tying you personally to the company’s obligations.

Critical Personal Risks for Foreign Legal Representatives

Beyond theoretical civil exposure, foreign legal representatives face three practical liability scenarios that can disrupt business operations and restrict personal freedom.

Exit ban risk

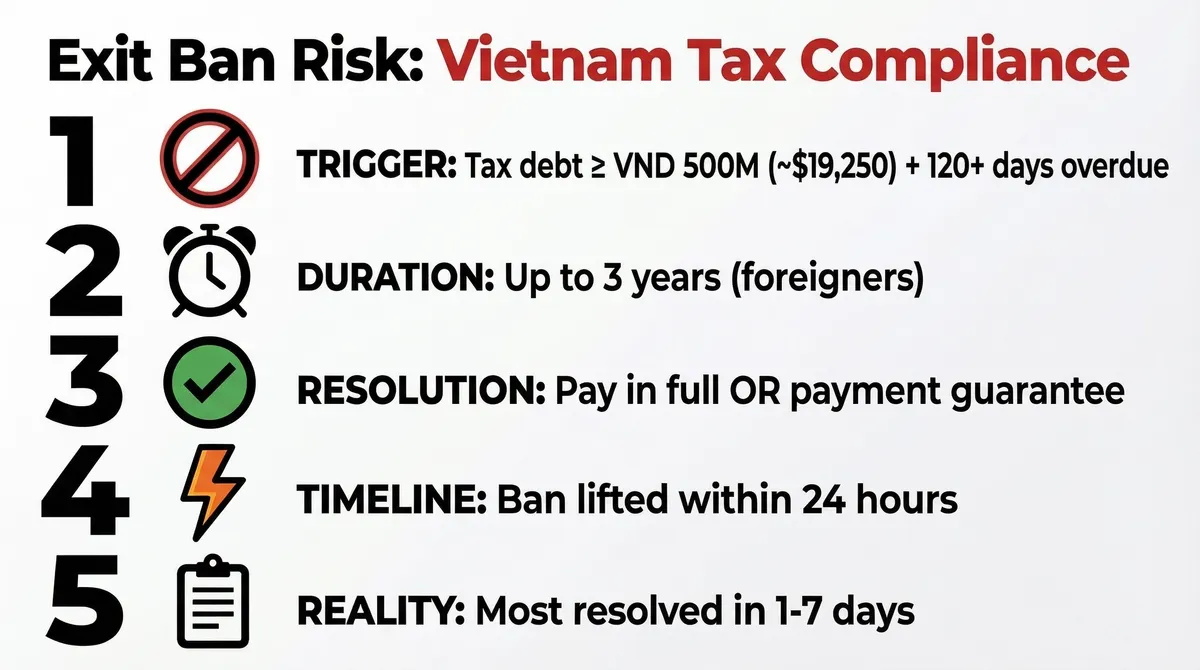

This is the scenario that keeps foreign legal representatives up at night. Tax authorities can prohibit you from leaving Vietnam when the company has outstanding tax obligations (Law on Tax Administration 2019, Article 66). Immigration authorities enforce this at the airport—you find out when you’re trying to board your flight.

How does this happen? Your accounting team makes a declaration error. A tax assessment comes in that the company disputes. An administrative penalty remains unpaid while you negotiate. Any of these can trigger a departure restriction request from tax authorities to immigration. The ban stays in place until the company satisfies the outstanding amount or provides adequate payment guarantees.

You don’t need to have personally caused the problem. Your name on the Enterprise Registration Certificate is enough.

The practical impact goes beyond travel disruption. While the exit ban is active, you can’t attend board meetings abroad, visit clients, or return home for personal matters. Resolution requires either full payment of the outstanding amount or negotiating a payment guarantee with tax authorities—a process that can take weeks when the company disputes the assessment.

Administrative and vicarious liability

Your signature on HR and payroll documents creates direct administrative exposure. Tax authorities and social insurance agencies treat your signature on declarations as approval—so when audits uncover non-compliance, the liability flows to you as the signing authority.

Work permit violations trigger immediate penalties. Organizations face fines from VND 60 million to VND 150 million (~USD 2,400–6,000) under Decree 12/2022/ND-CP, Article 32.4. Labor inspectors check work permit status during routine audits. No valid permit on file? Penalty assessment follows. Legal representative signatures on labor and social insurance declarations create direct exposure—for full employer obligations, see our Vietnam employment law and HR compliance framework for FDI employers.

Indirect criminal liability exposure

Customs declarations and import documentation carry criminal liability risk. While prosecution requires proof of intent, your signature authority on these documents creates investigative exposure—meaning legal defense costs and operational disruptions during inquiries, even when you’ve done nothing wrong.

The Dual Legal Representative Strategy

The dual legal representative model solves the core tension foreign investors face: you need someone in Vietnam handling daily compliance, but you can’t afford to hand over strategic control. Enterprise Law 2020, Article 12.1 permits companies to appoint multiple legal representatives—and this is where smart structuring starts.

DECISION TREE: Do You Need Dual Legal Representatives?

How to structure authority division

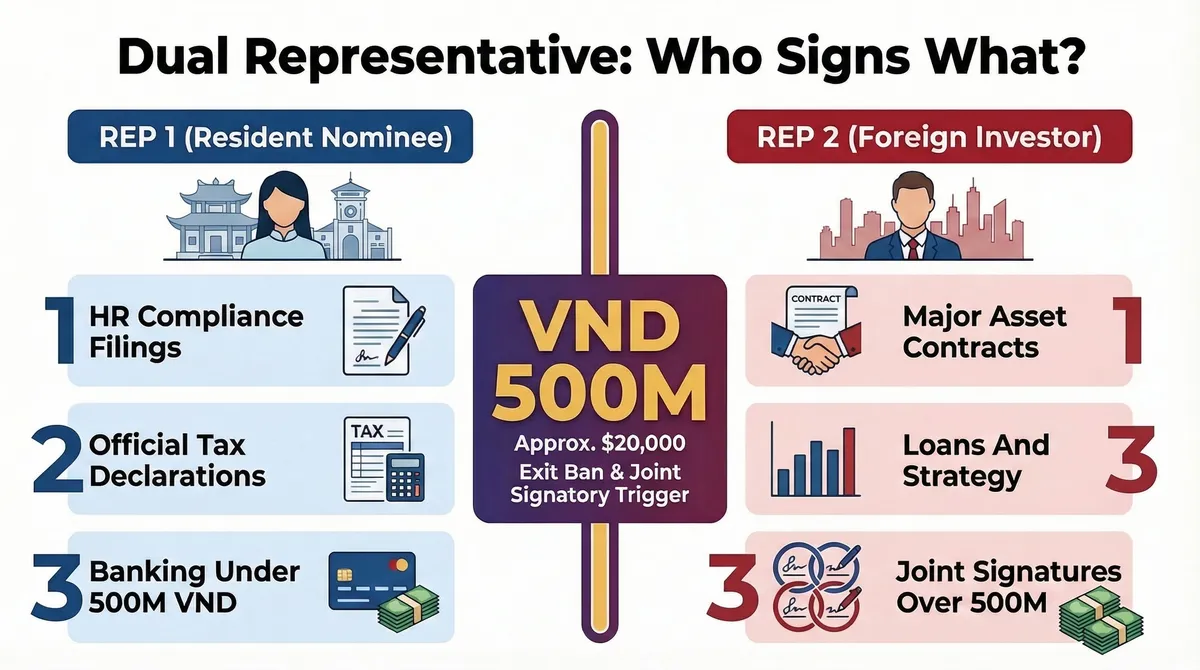

Appoint two legal representatives with explicitly divided authority in the Company Charter. The charter must specify which representative controls what:

- Legal Representative 1 (resident nominee): HR compliance, administrative filings, tax and social insurance declarations, banking transactions below specified thresholds

- Legal Representative 2 (foreign investor): Major asset transactions, contracts exceeding monetary thresholds, loan agreements, and strategic decisions requiring joint or exclusive signature

Set clear monetary thresholds in the charter. Routine transactions below VND 500 million (~USD 20,000) execute with the resident nominee’s signature alone. Anything above that threshold requires your authorization—or joint signatures from both representatives. The Company Charter governing this authority division follows the LLC governance structure, charter provisions, and ownership rules in Vietnam.

Solving residency compliance

Your resident legal representative ensures continuous compliance with the Article 12.3 residency mandate. You travel internationally without worrying about the 30-day authorization letter requirement, because the resident nominee maintains signature authority for time-sensitive filings. No operational paralysis when you’re abroad.

Segmenting administrative risk

Here’s the real value: the resident legal representative absorbs routine administrative exposure. Tax declaration signatures, social insurance filings, labor inspection responses—these all flow through the resident nominee. When tax authorities discover a declaration error, the initial liability exposure falls on the signing authority, not on you as the foreign investor sitting in Singapore or Tokyo.

This doesn’t eliminate your oversight responsibility. But it creates a structural buffer between daily compliance risk and your personal freedom to travel and operate across borders. If tax authorities impose a departure restriction, it targets the signing authority on the disputed declaration—not every legal representative on the company’s registration.

Maintaining control with appointed resident representatives

Foreign investors using appointed resident legal representative services maintain control through three mechanisms:

- Charter authority limits: The resident representative is restricted to administrative filings and transactions below defined thresholds (typically VND 500 million). Joint signature required for bank accounts, loans, asset disposals, and contracts above threshold.

- UBO transparency: The foreign investor remains registered as Ultimate Beneficial Owner regardless of the representative appointment—separating administrative authority from economic control. From July 2025, UBO disclosure becomes mandatory for anyone holding 25% or more ownership or control under Decree 168/2025/ND-CP—reinforcing the importance of clear authority division over informal arrangements.

- Service agreement protections: Professional representatives carry insurance, operate under formal agreements specifying scope and indemnity provisions—eliminating the labor dispute risks of internal staff appointments.

The appointed resident legal representative must also complete corporate e-ID registration under Decree 69/2024/ND-CP to access government portals for tax filings and regulatory submissions.

Warning: Appointing internal Vietnamese staff as legal representative creates control risks. During termination disputes, that staff member can refuse to sign documents or withhold the company seal—resolving this through the Business Registration Office takes a minimum of 15 working days, during which your company cannot execute contracts or file tax returns.

2025 Compliance Action Items

Two regulatory changes require immediate attention for foreign-invested companies:

Charter amendments (effective July 1, 2025): The 2025 Enterprise Law amendments require enhanced transparency in Company Charters. Review your current charter for legal representative provisions and authority division clauses. Submit amended charters to the Business Registration Office within 15 working days of any changes.

Work permit compliance (effective August 7, 2025): Foreign legal representatives must hold valid work permits or exemption certificates under Decree 219/2025/ND-CP. Submit applications to the Provincial People’s Committee (or Department of Home Affairs) where the company operates—either directly or through the National Public Service Portal. Labor inspectors verify work permit status during compliance reviews, and missing documentation triggers VND 60–150 million (~USD 2,400–6,000) penalties.

Don’t wait until inspection to discover a gap. Verify your work permit status and charter compliance now.

This information reflects regulations current as of January 2026. Vietnamese enterprise and tax laws change frequently. For specific situations, consult qualified legal and tax professionals licensed in Vietnam.

Indochina Link Vietnam provides legal representative structuring and company formation support, nominee services, and charter amendment guidance for foreign-invested companies. Questions about your personal liability exposure? We walk FDI companies through dual legal representative structures and 2025 compliance requirements daily.