Dissolving an FDI company in Vietnam takes 6-12 months and requires sequential clearance from four government agencies: the tax authority, DOLISA, customs (for EPE companies), and the Department of Finance (formerly DPI). Nothing moves in parallel — each step depends on the previous completion. For the full lifecycle from setting up a business in Vietnam through exit, dissolution is the final stage.

Tax finalization alone typically consumes 3-6 months. The provincial tax authority conducts a full audit covering all outstanding tax periods before issuing clearance. No clearance = no deregistration.

Companies that try to shortcut the process discover that the legal representative bears personal liability for unresolved obligations even after the company ceases operations.

Key takeaways

- 6-12 months minimum from dissolution resolution to final deregistration.

- Tax finalization audit (3-6 months) is the critical path — no shortcutting.

- Employee settlement: Employment contracts terminate upon dissolution (Labor Code Article 34). Severance: 0.5 month salary per year of service (Article 46).

- EPE companies must clear bonded goods through customs before tax finalization.

- Legal representative remains liable until deregistration — personal exit planning matters.

The Dissolution Timeline

| Phase | Duration | Key Activities |

|---|---|---|

| 1. Resolution | Week 1 | Board/member resolution, dissolution committee formation |

| 2. Notification | Week 2-4 | Public announcement, creditor notification, employee notice |

| 3. Employee settlement | Month 1-2 | Severance payments, SHUI closeout, DOLISA reporting |

| 4. Asset liquidation | Month 2-4 | Equipment sale, lease termination, accounts receivable collection |

| 5. Tax finalization | Month 3-9 | Tax audit, CIT/VAT/PIT settlement, clearance certificate |

| 6. Customs clearance (EPE) | Month 3-5 | Bonded goods reconciliation, duty payment on unsold inventory |

| 7. Deregistration | Month 6-12 | Department of Finance (formerly DPI) filing, seal destruction, bank account closure |

Phase 1: Dissolution Resolution

Prerequisites before the resolution: all branches, representative offices, and affiliated business locations must be closed first — the parent entity cannot dissolve while subsidiaries remain active. The company must not be party to any pending court case or arbitration. Foreign investors who will not be present in Vietnam during the process should arrange a notarized Power of Attorney (POA) — consularized if executed abroad.

The Member’s Council (LLC) or General Meeting of Shareholders (JSC) passes a dissolution resolution (Enterprise Law 59/2020/QH14, Articles 207–208). The resolution must specify:

- Reason for dissolution

- Timeline for asset liquidation and debt settlement

- Dissolution committee composition and authority

- Plan for employee settlement

Phase 2: Creditor and Public Notification

Within 7 days of the resolution:

- File dissolution notice with the Department of Finance (formerly DPI)

- Publish dissolution announcement on the National Public Service Portal (Cổng Dịch vụ công Quốc gia)

- Send written notice to all known creditors with payment schedule

- Post dissolution notice at the company’s registered office

The dissolution remains open for 180 days from the resolution date for stakeholder objections (Enterprise Law 59/2020/QH14, Article 208). The dissolution committee reviews and resolves creditor claims and distributes assets according to the statutory priority: dissolution costs → employee wages and benefits → tax obligations → trade creditors → remaining assets to investors.

Phase 3: Employee Settlement

Dissolution triggers the termination of all pending employment contracts (Labor Code 45/2019/QH14, Article 34). Companies must settle employment obligations:

- Severance payment: 0.5 month of average salary per year of service applies for employees with 12+ months of continuous employment (Article 46)

- Employee notification: Companies must notify employees in writing regarding the termination of their employment contracts (Article 45)

- Unemployment insurance: employees with 12+ months of UI contribution qualify for unemployment benefits — the company facilitates applications before account closure

- Social Insurance account closure: finalize all SHUI contributions, close employer accounts, and return Social Insurance books to each employee

For foreign employees: work permits are cancelled at DOLISA. Temporary residence cards must be returned to immigration authorities. Work permit cancellation should happen before the company’s deregistration — processing afterward becomes significantly harder.

Phase 4: Asset Liquidation

Sell or transfer all company assets:

- Fixed assets (machinery, equipment, vehicles) — at market value or below with proper documentation

- Inventory and raw materials

- Accounts receivable — collect or write off

- Office lease — terminate per lease agreement terms (early termination penalties may apply)

For manufacturing companies with specialized equipment, asset sales to other FDI companies in the same industrial zone are common. Industrial zone management boards may facilitate introductions.

Phase 5: Tax Finalization

The most time-consuming phase. The provincial tax authority conducts a full audit covering:

- CIT: Final-year CIT return plus reconciliation of all prior open periods

- VAT: Final VAT return, input tax credit verification, and pending refund resolution

- PIT: Final PIT withholding reconciliation and annual finalization for all employees

- FCT: Verification of all foreign contractor tax withholding

VAT refund during dissolution: if the company has accumulated input VAT credits (common for manufacturing FDI), the refund application runs concurrently with the tax audit — but adds approximately 40 working days to the timeline. The tax authority will not issue the finalization certificate until the refund is either paid or waived.

The tax authority issues a tax finalization certificate (Xác nhận hoàn thành nghĩa vụ thuế) only after all obligations are settled — including any penalties and interest from audit findings.

Typical duration: 3-6 months, though clean cases can clear in 60-90 days. Complex cases extend to 120+ days. Common delays: transfer pricing adjustments triggering additional CIT, unresolved VAT refund claims, and missing documentation for prior-year deductions.

Phase 6: Customs Clearance (EPE Companies)

EPE companies face additional requirements:

- Finalize bonded goods inventory with customs authorities

- Pay import duty + VAT on any bonded raw materials or finished goods not exported

- Settle customs-related obligations (fines, penalties, or disputes)

- Obtain customs clearance certificate

This runs concurrently with tax finalization but must complete before deregistration.

Phase 7: Deregistration

With tax finalization certificate, customs clearance (if applicable), and debt settlement evidence in hand:

- Submit deregistration application to the Department of Finance (formerly DPI)

- The Department of Finance publishes deregistration notice on the National Public Service Portal (Cổng Dịch vụ công Quốc gia) (5 working days)

- Destroy the corporate seal per police notification (within 10 days)

- Close all bank accounts

- Return digital certificates and cancel e-ID registration

The entity ceases to exist at the date the Department of Finance issues the deregistration confirmation.

What Dissolution Costs

No government fee is charged for the dissolution filing itself, but professional and operational costs add up:

| Cost Component | Typical Range |

|---|---|

| Accounting/tax advisory fees (finalization support) | VND 30–60 million (~USD 1,200–2,400) |

| Legal fees (filings, POA, seal destruction) | VND 10–20 million (~USD 400–800) |

| Employee severance (varies by headcount) | 0.5 month salary × years of service × headcount |

| Tax penalties/interest (if audit findings) | Variable — can exceed VND 100 million for multi-year issues |

| Asset liquidation costs (valuation, transport) | VND 5–15 million (~USD 200–600) |

Total professional costs for a typical small-to-medium FDI company (10–30 employees, 3–5 years of operation): VND 50–100 million (~USD 2,000–4,000) excluding severance and tax penalties.

After Deregistration — Remaining Obligations

Deregistration does not end all obligations:

- Accounting records retention: 10 years from the date of deregistration (Accounting Law 88/2015/QH13, Article 41). Tax authorities can audit dissolved entities within this period.

- Capital repatriation: remaining funds in the Direct Investment Capital Account (DICA) can only be remitted abroad after the bank receives the tax finalization certificate and deregistration confirmation. The bank closes the DICA and transfers the balance to the investor’s overseas account — forex conversion at the commercial bank’s selling rate on the transfer date.

- IRC/ERC status: the IRC and ERC amendments related to dissolution are final — the certificates are revoked, not amended.

Common Pitfalls — When Sequence Goes Wrong

Dissolution phases must complete in order. Skipping ahead creates cascading problems:

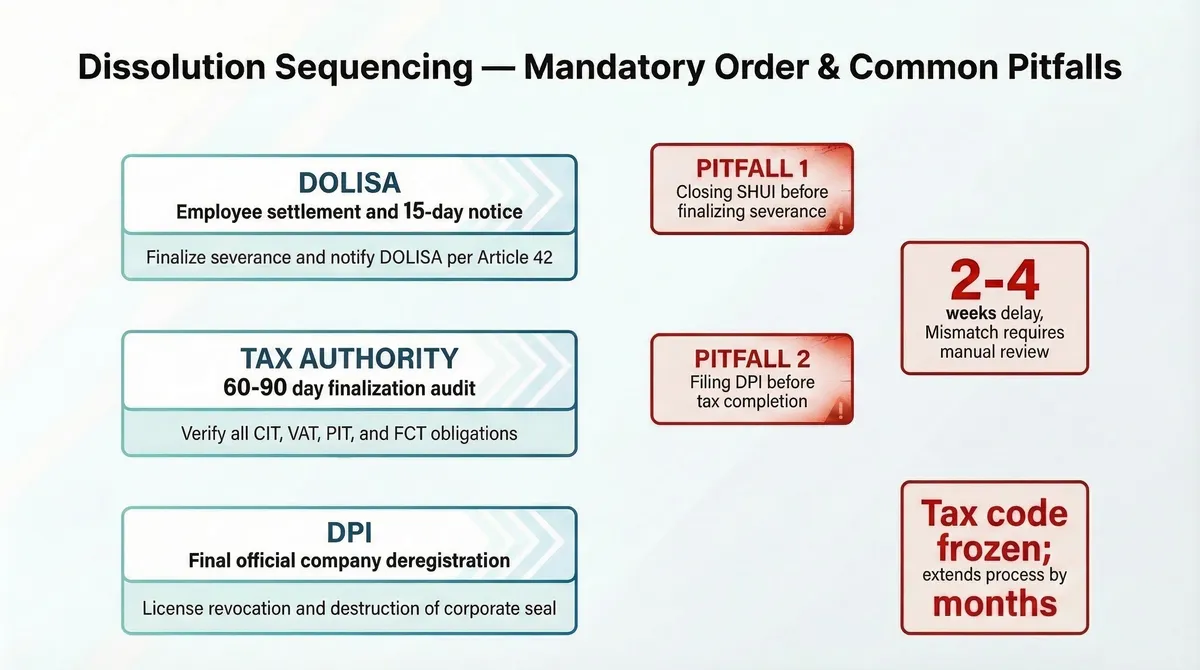

Tax code freeze: filing the dissolution application at the Department of Finance (formerly DPI) triggers a status change on the National Public Service Portal (Cổng Dịch vụ công Quốc gia). Once the tax code shows “đang giải thể” (dissolving), the company can no longer file supplementary tax returns or amended declarations. FDI companies that submit dissolution paperwork before completing tax finalization find themselves unable to resolve audit findings — extending the process by months.

SHUI account mismatch: closing Social Insurance accounts before finalizing employee severance creates reconciliation errors at DOLISA. The corrected Social Insurance books must match the final payroll records exactly — discrepancies require manual review that adds 2–4 weeks.

Customs bond release: EPE companies that liquidate bonded goods before obtaining customs clearance face duty reassessment on the full inventory value — not just remaining stock. Starting Phase 4 (asset liquidation) before Phase 6 (customs) is a costly sequencing error.

For tax finalization support, dissolution advisory, and exit planning — contact the compliance team. David Nguyen coordinates corporate restructuring and dissolution for FDI companies, working with the certified CPAs on tax clearance and SHUI closeout.

This guide reflects dissolution procedures as of March 2026 under the Enterprise Law (Law 59/2020/QH14), Investment Law (Law 61/2020/QH14, as amended by Law 90/2025/QH15), Labor Code (Law 45/2019/QH14), and Tax Administration Law (Law 38/2019/QH14). Procedures are subject to changes in implementing regulations — consult qualified legal and tax advisors before initiating dissolution.