Vietnamese FDI M&A transactions process through the Department of Finance (formerly DPI) within 15 to 35 working days. Buyers can structure deals through share acquisitions, capital contributions, or asset purchases. Each legal structure triggers vastly different tax liabilities under Vietnam’s M&A tax framework (Decree 320/2025/ND-CP).

Share deals are the most common FDI route. Why? Because the target continues operations without disruption. The buyer simply acquires equity in the Vietnamese entity, instantly inheriting all underlying assets, contracts, and operating licenses. But there’s a serious catch. The buyer undeniably inherits all historical tax and compliance liabilities as well. Before crossing the 49% or 51% foreign ownership thresholds in restricted industries, rigorous due diligence is non-negotiable. M&A is one of three pathways in the Vietnam market entry roadmap, serving as the fastest route to direct market access.

Key takeaways

- Three M&A structures: share acquisition (most common), capital contribution, asset acquisition.

- Share deals: buyer inherits all liabilities. Asset deals: buyer acquires clean assets. Structure heavily determines risk.

- Registration at the Department of Finance is mandatory whenever foreign ownership percentages change or conditional sectors are involved.

- Capital gains tax (Decree 320/2025): foreign corporate sellers pay 2% on gross proceeds; Vietnamese corporates pay 20% on net gains.

- Structuring an M&A deal blindly is dangerous — tax due diligence is absolutely non-negotiable because contingent liabilities transfer upon closing.

M&A Structures Compared

| Factor | Share Acquisition | Capital Contribution | Asset Acquisition |

|---|---|---|---|

| What changes | Ownership of equity | New member/shareholder added | Ownership of specific assets |

| IRC treatment | Amendment | Amendment | No change to target |

| Target entity continues | ✅ Yes | ✅ Yes | Target continues (minus assets) |

| Liabilities transfer | ✅ All historical | ✅ All historical | ❌ Seller retains |

| Contracts transfer | ✅ Automatic | ✅ Automatic | Requires assignment |

| Employee transfer | ✅ Automatic | ✅ Automatic | Article 29 novation |

| Tax implications (buyer) | Inherits tax positions | Inherits tax positions | No inheritance |

| Tax implications (seller) | 2% gross (foreign corp) / 20% net (VN corp) | N/A (dilution, not sale) | CIT on asset gain |

| Timeline | 15-35 days (Department of Finance (formerly DPI)) | 15-35 days (Department of Finance (formerly DPI)) | 30-60 days (contract-based) |

Share Acquisition

The buyer purchases existing shares/capital contributions from the current owner. The target company’s IRC, licenses, contracts, and employment relationships continue uninterrupted.

When to use: acquiring an operating company with existing revenue, licenses, and workforce. Most FDI M&A transactions in Vietnam follow this structure — it preserves the target’s established relationships, tax history, and operational permissions.

Risk: the buyer inherits all historical liabilities. Uncovered tax obligations, pending legal disputes, and unresolved licensing compliance issues all become the buyer’s direct problem post-closing.

Capital Contribution

A new investor contributes additional capital to the target company, becoming a member/shareholder. Existing ownership is diluted proportionally. No direct payment goes to existing shareholders — the capital goes directly into the company itself.

When to use: strategic investment without full acquisition. The new investor gains board representation and operational influence proportional to their contribution.

Asset Acquisition

The buyer purchases specific assets (machinery, real estate, IP, contracts) from the target. The target company continues to exist — minus the transferred assets.

When to use: acquiring specific production capacity, real estate, or IP without inheriting the entity’s history. It is generally more complex due to individual asset transfer formalities, but much cleaner from a liability perspective.

Regulatory Process: Department of Finance (formerly DPI) Registration

When Department of Finance Registration Is Required

Department of Finance (formerly DPI) registration is mandatory when:

- A foreign investor acquires shares/capital in a Vietnamese company for the first time (thereby creating FDI status)

- An existing foreign investor’s ownership percentage changes

- The transaction involves a conditional business line under special foreign ownership restrictions

- The target company holds land use rights, operates in sensitive sectors (defense, publishing, telecommunications), or has access to national security resources

Registration Documents

Standard dossier for share acquisition:

- Share/capital transfer contract between buyer and seller

- Target company’s current IRC and ERC (certified copies)

- Buyer’s incorporation documents (legalized, notarized)

- Investment project proposal (for first-time FDI registration)

- Resolution of the target company’s members/shareholders approving the transfer

- Financial statements of the target company (most recent audited year)

- Proof of buyer’s financial capacity (bank statements, parent company guarantee)

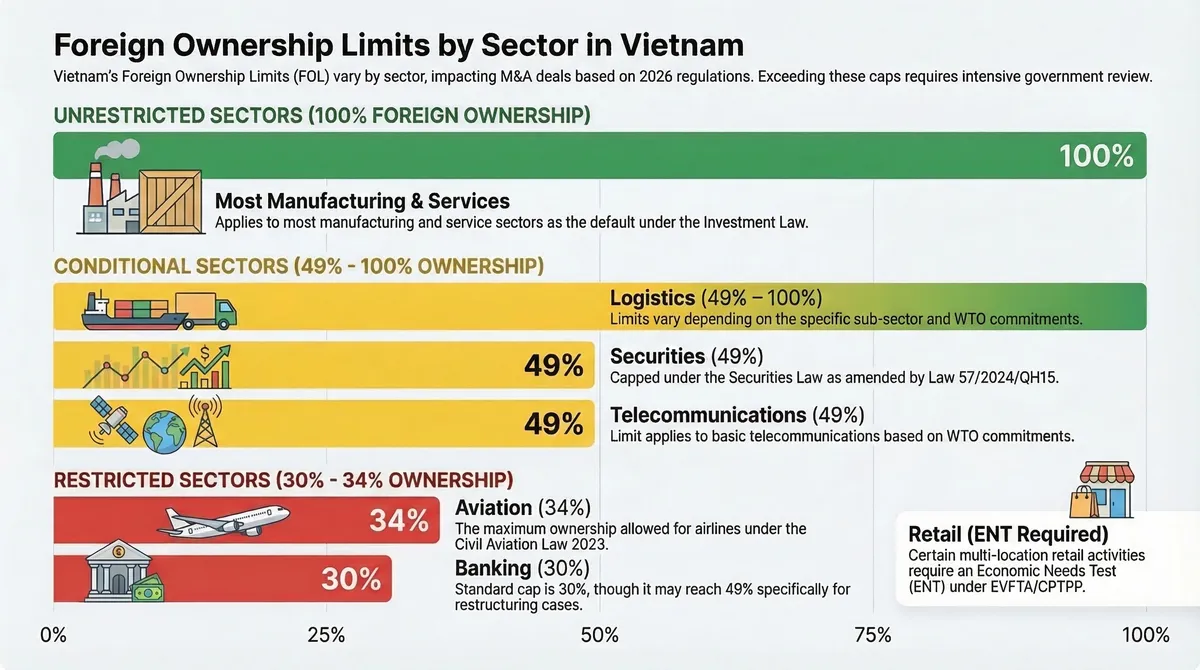

Foreign Ownership Limits

Vietnam maintains strict, sector-specific foreign ownership restrictions:

| Sector | Maximum Foreign Ownership | Basis |

|---|---|---|

| Unrestricted sectors | 100% | Default under Investment Law |

| Banking | 30% (49% for restructuring) | Law on Credit Institutions 2024 (Law 32/2024/QH15) |

| Telecommunications (basic) | 49% | WTO commitments |

| Aviation | 34% (airlines) | Civil Aviation Law 2023 (Law 68/2023/QH15) |

| Securities | 49% | Securities Law (as amended by Law 57/2024/QH15) |

| Retail (multi-location) | Requires ENT | EVFTA, CPTPP commitments |

| Logistics | 49–100% (varies by sub-sector) | WTO commitments |

Before initiating an M&A transaction, verify the applicable foreign ownership limit for the target’s specific VSIC codes. Some limits are currently being progressively relaxed under FTA commitments (EVFTA, CPTPP, RCEP).

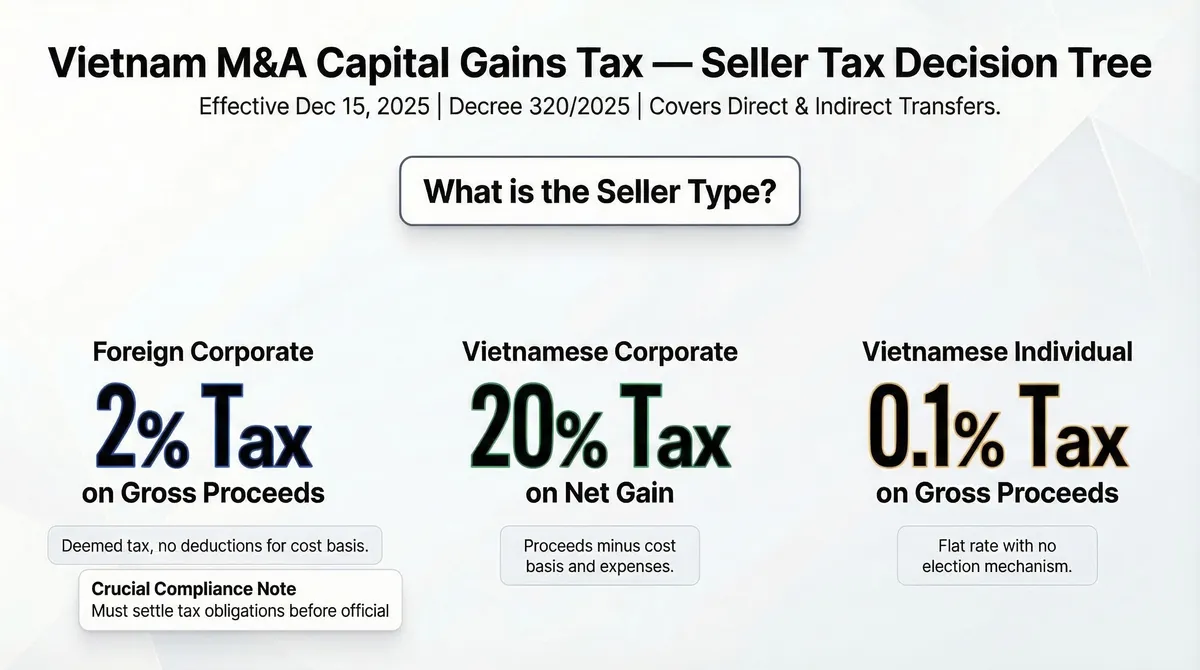

Tax Implications

Capital gains taxation on share transfers was fundamentally restructured under Decree 320/2025/ND-CP (effective 15 December 2025). The tax treatment heavily depends on the seller’s status:

For the Seller

| Seller Type | Tax Rate | Tax Base | Notes |

|---|---|---|---|

| Foreign corporate | 2% | Gross proceeds | Deemed tax — no deductions for cost basis |

| Vietnamese corporate | 20% | Net gain (proceeds − cost basis − expenses) | Standard CIT treatment |

| Individual (LLC Capital) | 20% | Net gain (proceeds − cost basis − expenses) | Standard treatment for most FDI entities |

| Individual (JSC Shares) | 0.1% | Gross proceeds | Flat rate, regardless of profit |

Foreign corporate sellers must settle tax obligations before the Enterprise Registration Authority updates shareholder records. The seller — not the buyer — is responsible for all declarations and payments.

Indirect Transfers

Indirect capital transfers — where an offshore holding company transfers ownership of a Vietnamese subsidiary — are now formally recognized and taxed under Decree 320/2025 (Article 12). Foreign corporate sellers pay 2% CIT on the portion of proceeds strictly attributable to Vietnamese assets. This finally closes a gap that previously made offshore restructuring a common tax minimization strategy.

For the Buyer

No direct acquisition tax applies on share purchases. Key considerations:

- Stamp duty may apply on asset transfers within the deal (land use rights, vehicles)

- Goodwill amortization: if the purchase price exceeds net asset value, goodwill is amortized over 10–20 years for CIT purposes

- Inherited tax positions: all of the target’s CIT incentives, carried-forward losses, VAT positions, and pending tax audit findings fundamentally transfer to the buyer

Transfer Pricing

Related-party transactions are uniquely subject to transfer pricing scrutiny under Decree 132/2020/ND-CP. The acquisition price must reflect arm’s-length value, which means independent valuation reports are essential transaction documentation.

What M&A Transactions Cost

Professional and regulatory costs for a typical FDI share acquisition:

| Cost Component | Typical Starting Point |

|---|---|

| Legal advisory (SPA drafting, Department of Finance (formerly DPI) filing) | From VND 50 million+ (~USD 2,000+) |

| Tax advisory and structuring | From VND 30 million+ (~USD 1,200+) |

| Financial/tax due diligence | From VND 50 million+ (~USD 2,000+) |

| Independent asset valuation | From VND 20 million+ (~USD 800+) |

| Capital gains tax (seller) | 2% of gross proceeds (foreign corp) |

Fees scale dramatically with deal complexity. The number of entities, cross-border structures, and sector-specific licensing all dictate the final scope. For a typical small-to-mid-size deal, total professional costs start from VND 150 million+ (~USD 6,000+) (excluding the transaction price and seller tax obligations). Larger or multi-entity transactions require completely separate scoping.

Cost estimates above reflect typical market ranges based on our transaction advisory experience and are indicative only. Actual fees reliably depend on deal scope and complexity.

Due Diligence Red Flags

Share acquisitions transfer all historical liabilities straight to the buyer. These issues consistently delay or kill FDI deals in Vietnam:

- Pending tax audit or unresolved tax disputes — the target’s tax exposure immediately becomes the buyer’s risk on closing day.

- SHUI underpayment or misclassification — Social Insurance arrears carry daily penalties of 0.03% and can instantly trigger criminal liability for the legal representative.

- Land lease irregularities — expired leases, unauthorized subletting, or land-use purpose mismatches with the IRC.

- Undisclosed related-party contracts — off-market pricing generates brutal transfer pricing exposure retroactive to the transaction date.

- Outstanding employee disputes or unpaid wages — unresolved labor claims and severance obligations smoothly transfer to the buyer, carrying DOLISA enforcement risk.

A highly structured tax due diligence process identifies these exposures before the SPA is ever drafted or signed. For complex transactions — particularly manufacturing targets or companies with multi-year tax audit gaps — you must engage independent advisors early.

Post-Acquisition Integration

After the transaction closes and IRC/ERC amendments are completed:

| Action | Timeline | Notes |

|---|---|---|

| IRC amendment | 15–35 days | Reflects new investor identity |

| ERC amendment | 3–5 days | Updates legal representative, charter |

| Tax authority notification | 10 working days | Update tax registration |

| Bank account signatory update | Varies | New authorized signatories |

| Employee notification | Immediate | Labor Code 2019 requires notice |

| SHUI account update | 30 days | If legal entity details change |

| Customs registration update (EPE) | 10 days | If investor of record changes |

Capital flow: the buyer’s investment funds must enter Vietnam through the Direct Investment Capital Account (DICA) at a Vietnamese commercial bank. The bank predictably releases payment to the seller’s account only after receiving the amended IRC confirming the ownership transfer — ensuring strict regulatory compliance before any funds physically move.

For M&A transaction advisory, regulatory share transfer registration, and post-acquisition restructuring — our Corporate M&A team comprehensively manages cross-border transfers and due diligence for FDI companies.

This guide reflects M&A regulations as of March 2026 under the Investment Law (Law 61/2020/QH14, as amended by Law 90/2025/QH15), Decree 168/2025/ND-CP, Decree 320/2025/ND-CP, and Tax Administration Law (Law 38/2019/QH14). Foreign ownership limits and sector restrictions are subject to FTA-driven changes — verify current thresholds before structuring transactions.