Changing investment capital in a Vietnamese FDI company requires amending the Investment Registration Certificate (IRC) followed by the Enterprise Registration Certificate (ERC). The Department of Finance (formerly DPI) processes IRC amendments within 15 to 35 working days, taking another 3 to 5 days for the ERC update. Investors must provide a clear contribution schedule for increases or proof of debt clearance for decreases.

FDI companies typically adjust their capital within their first five years. Whether scaling production, expanding into new lines, or restructuring, this is a standard part of the business setup lifecycle in Vietnam. But it comes with strict compliance traps. Missed contribution deadlines trigger enforcement under the Enterprise Law, and dropping below investment thresholds can instantly void Corporate Income Tax (CIT) incentives.

Key takeaways

- Both IRC and ERC amendments required at the Department of Finance. IRC amendment (15-35 days) precedes ERC amendment (3-5 days).

- New capital must arrive within 90 days of ERC issuance. Missed deadlines trigger immediate enforcement (Enterprise Law 59/2020/QH14, Article 75).

- Profits convert to charter capital via retained earnings capitalization, requiring no fresh cash injection.

- Capital decreases mandate complete debt settlement proof before the authorities grant approval.

- Changing registered capital alters CIT holiday calculations and incentive qualification thresholds.

Capital Increase

Why FDI Companies Increase Capital

Capital increases serve distinct business purposes:

Operational expansion: financing new production lines, additional facilities, or market expansion within Vietnam. Manufacturing FDI in industrial zones frequently increase capital for capacity upgrades.

Working capital needs: charter capital determines borrowing capacity and may affect the ratio of debt-to-equity under State Bank of Vietnam regulations for foreign borrowing.

Regulatory requirements: some conditional sectors require minimum legal capital. Growth beyond certain thresholds may trigger re-evaluation of capital adequacy.

Retained earnings capitalization: converting accumulated profits into charter capital rather than repatriating dividends. This is a common strategy for FDI companies reinvesting in Vietnam operations.

Capital Increase Process

Step 1: Internal Resolution

The Member’s Council (LLC) or General Meeting of Shareholders (JSC) passes a resolution to increase capital, specifying:

- New total investment capital and charter capital amounts

- Source of additional capital (foreign remittance, retained earnings, additional investor)

- Capital contribution schedule

- Amended business plan justifying the increase

Step 2: IRC Amendment at Department of Finance (15-35 working days)

File with the provincial Department of Finance (formerly DPI):

| Document | Notes |

|---|---|

| Application for IRC amendment | Standard form per Circular 03/2021/TT-BKHDT |

| Resolution of members/shareholders | Notarized |

| Updated investment project financial plan | Showing deployment of additional capital |

| Proof of capital source | Bank statements, parent company board resolution, audited financials |

| Current IRC (certified copy) | For reference |

The Department of Finance reviews the capital utilization rate of the existing investment. Have you fully deployed the original capital? They also evaluate the justification for the increase and any sector-specific capital requirements.

Step 3: ERC Amendment at Department of Finance (3-5 working days)

After IRC amendment is issued, file the ERC amendment reflecting the new charter capital figure.

Step 4: Complete Capital Contribution

The actual capital must be transferred within the schedule specified in the amended IRC. For cash contributions from overseas: wire transfer to the Direct Investment Capital Account (DICA) at the company’s Vietnamese bank. The bank records the contribution and reports to the State Bank of Vietnam.

Capital Contribution Schedule Enforcement

Charter capital must be contributed strictly according to the schedule registered in the ERC (Enterprise Law 59/2020/QH14, Article 75). For new companies, the initial contribution must be completed within 90 days of ERC issuance. For capital increases, the contribution timeline follows the schedule specified in the amended IRC — typically 90 days from amendment approval.

If the contribution isn’t completed on schedule:

- Department of Finance written reminder — requesting timeline for completion

- Adjusted IRC — scaling down charter capital to match actual contributions, reducing total investment capital proportionally

- CIT incentive recalculation — if incentives were based on a larger capital amount, the qualification threshold may no longer be met

- Voting rights reduction — for JSCs, uncontributed shares may be cancelled. For LLCs, member voting rights adjust proportionally to actual contributions (Enterprise Law 59/2020/QH14, Article 47)

In practice, the Department of Finance typically issues one written reminder before taking formal action. FDI companies that demonstrate partial progress — such as placing equipment orders or signing construction contracts — often receive schedule extensions. The enforcement escalation basically unfolds over 6-12 months, not immediately upon schedule expiration.

Funding Sources

| Source | Requirements | Documentation |

|---|---|---|

| Foreign remittance from parent | Wire to DICA, forex bank confirmation | Bank credit advice, SWIFT confirmation |

| Retained earnings | Resolution to capitalize, no outstanding tax obligations | Audited financial statements, tax clearance |

| Additional new investor | M&A/share transfer registration process first | New investor admission documents |

| Equipment contribution in-kind | Independent valuation, customs clearance | Valuation report, import documentation |

Equipment contributions (in-kind capital) require independent valuation by a licensed Vietnamese valuation firm. Customs clearance documentation must match the valuation. Any discrepancies immediately trigger both customs and tax authority inquiries.

Capital Decrease

When FDI Companies Decrease Capital

Capital decrease is less common than increases but serves specific restructuring needs:

Reflecting accumulated losses: years of losses may leave charter capital overstated relative to actual net assets. Reducing capital to match economic reality eliminates the gap between registered and actual equity. Auditors and tax authorities heavily flag this gap during inspections.

Business downsizing: scaling back operations, exiting product lines, or reducing footprint within Vietnam. Lower charter capital aligns with reduced operational scope and may lower future reporting obligations.

Investor exit: when one member exits and remaining members choose not to fully replace that member’s capital contribution, charter capital decreases proportionally.

Post-acquisition restructuring: after acquiring a Vietnamese entity, foreign investors sometimes reduce inflated charter capital from the previous ownership structure to align with actual operational needs.

Capital Decrease Process

The Department of Finance applies heightened scrutiny for capital decreases to protect creditors and employees.

LLC capital decrease follows the Enterprise Law 59/2020/QH14 (Article 68): the Members’ Council passes a resolution to reduce charter capital, updates the company charter, and files the ERC amendment within 10 working days of the resolution.

JSC capital decrease under Article 112 can occur through: (a) returning contributed capital proportionally to shareholders, (b) buying back issued shares, or (c) adjusting charter capital to reflect actual paid-in amounts after the contribution period expires.

Required documents for IRC/ERC amendment:

- Resolution to decrease charter capital with justification

- Latest audited financial statements showing net asset position

- Written confirmation that all debts are settled or adequately provisioned

- Tax clearance or confirmation of no outstanding tax obligations

- Employee confirmation: no outstanding severance or SHUI obligations

- Updated investment project plan reflecting reduced scope

Evaluation criteria by the Department of Finance:

- Are all financial obligations settled — including tax, SHUI, and trade creditors?

- Is the remaining capital sufficient for continued operations under the declared business activities?

- Are there any pending labor disputes or outstanding employee entitlements?

- Does the decrease affect any conditional business line minimum capital requirements?

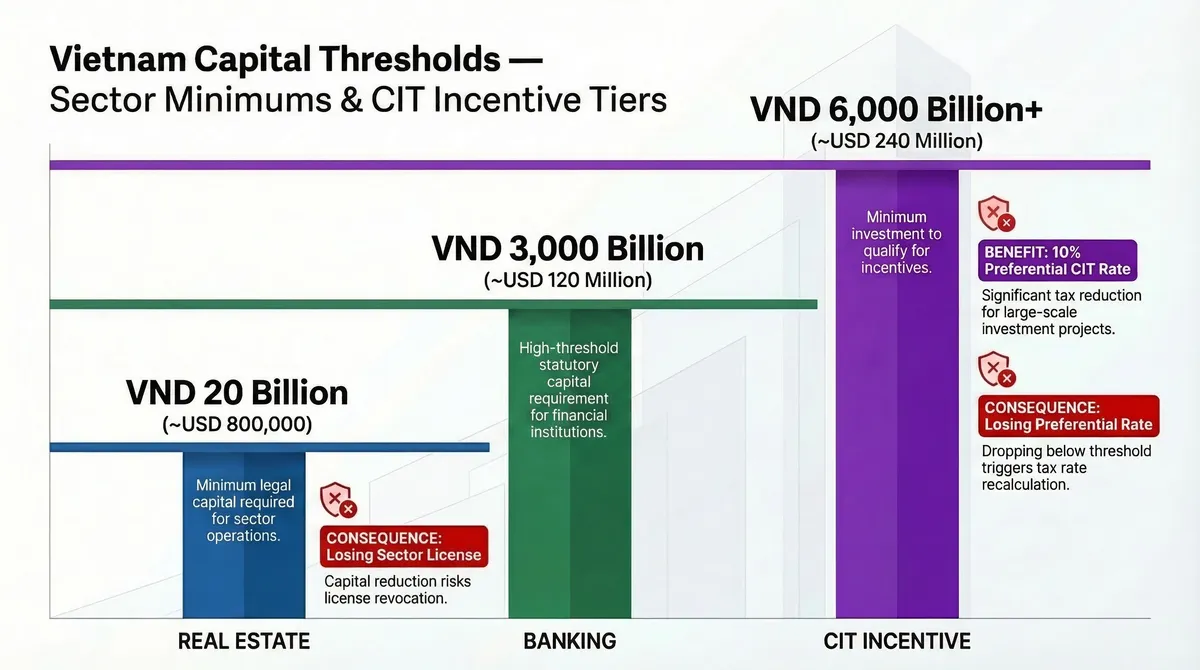

Common rejection reasons: insufficient documentation of debt settlement, ongoing tax audit or unresolved tax dispute, or remaining capital dropping below sector-specific minimum thresholds (banking: VND 3,000 billion / ~USD 120 million; real estate: 15-20% of the project’s total investment capital).

Processing time: 15-35 working days for IRC amendment, plus 3-5 days for ERC amendment.

Tax and Compliance Implications

CIT Incentive Impact

Capital changes directly affect CIT incentive qualification:

- Tax holiday calculations tied to investment capital thresholds may be recalculated

- Encouraged sector qualification based on total investment may change

- Zone incentive requirements specifying minimum investment amounts

Review CIT incentive conditions before initiating capital changes. A capital decrease that drops below the incentive threshold may affect future procedures — including tax refund applications, new investment registrations, and other incentive-related filings.

For example, an FDI manufacturing company enjoying a 10% CIT rate based on total investment exceeding VND 6,000 billion (~USD 240 million) would lose that preferential rate immediately if a capital decrease brings total investment below the threshold.

Business License Tax — Abolished from 2026

The Business License Tax (BLT) — previously tiered by charter capital at VND 1–3 million annually — was completely abolished effective January 1, 2026 (Resolution 198/2025/QH15, implemented by Decree 362/2025/ND-CP). Consequently, capital changes no longer trigger BLT tier adjustments, permanently removing one compliance step from the amendment process.

FDI companies that paid BLT for 2025 or earlier should verify final settlement with the district tax authority. Any overpayments are fully creditable against other tax obligations.

Foreign Loan Capacity

The State Bank of Vietnam limits net short-term and medium/long-term foreign borrowing based on capital structure. Capital increases expand foreign borrowing capacity; decreases contract it. If the company has outstanding registered foreign loans, capital changes require SBV notification.

A capital increase from VND 50 billion (~USD 2 million) to VND 150 billion (~USD 6 million) effectively triples the company’s borrowing headroom for medium/long-term foreign loans. This is a significant consideration for FDI companies financing expansion through parent company loans.

Post-Amendment Actions

After capital change IRC/ERC amendments are completed:

- Update tax registration — notify the district tax authority within 10 working days

- Update bank account — DICA account authority may need adjustment at the commercial bank

- Notify SBV — if the company holds foreign loan registrations

- Update insurance — directors’ and officers’ liability insurance (if held) may reference capital amounts

- File next periodic report — updated capital in the quarterly investment activity report

Capital decreases during company dissolution follow a separate exit process with additional tax clearance requirements.

For corporate amendment filings including capital changes, IRC/ERC coordination, and post-amendment compliance — our Corporate Structuring & Compliance team handles complete capital restructuring and regulatory coordination for FDI companies.

This guide reflects capital change procedures as of March 2026 under the Investment Law 61/2020/QH14 (as amended by Law 90/2025/QH15), Enterprise Law (Law 59/2020/QH14), and Decree 168/2025/ND-CP on enterprise registration. Procedures and capital requirements may change with sector-specific regulations — consult qualified legal and tax advisors for current requirements.